What San Francisco Luxury Buyers Need to Know in 2026

Sean Mamola | March 5, 2026

Sean Mamola | March 5, 2026

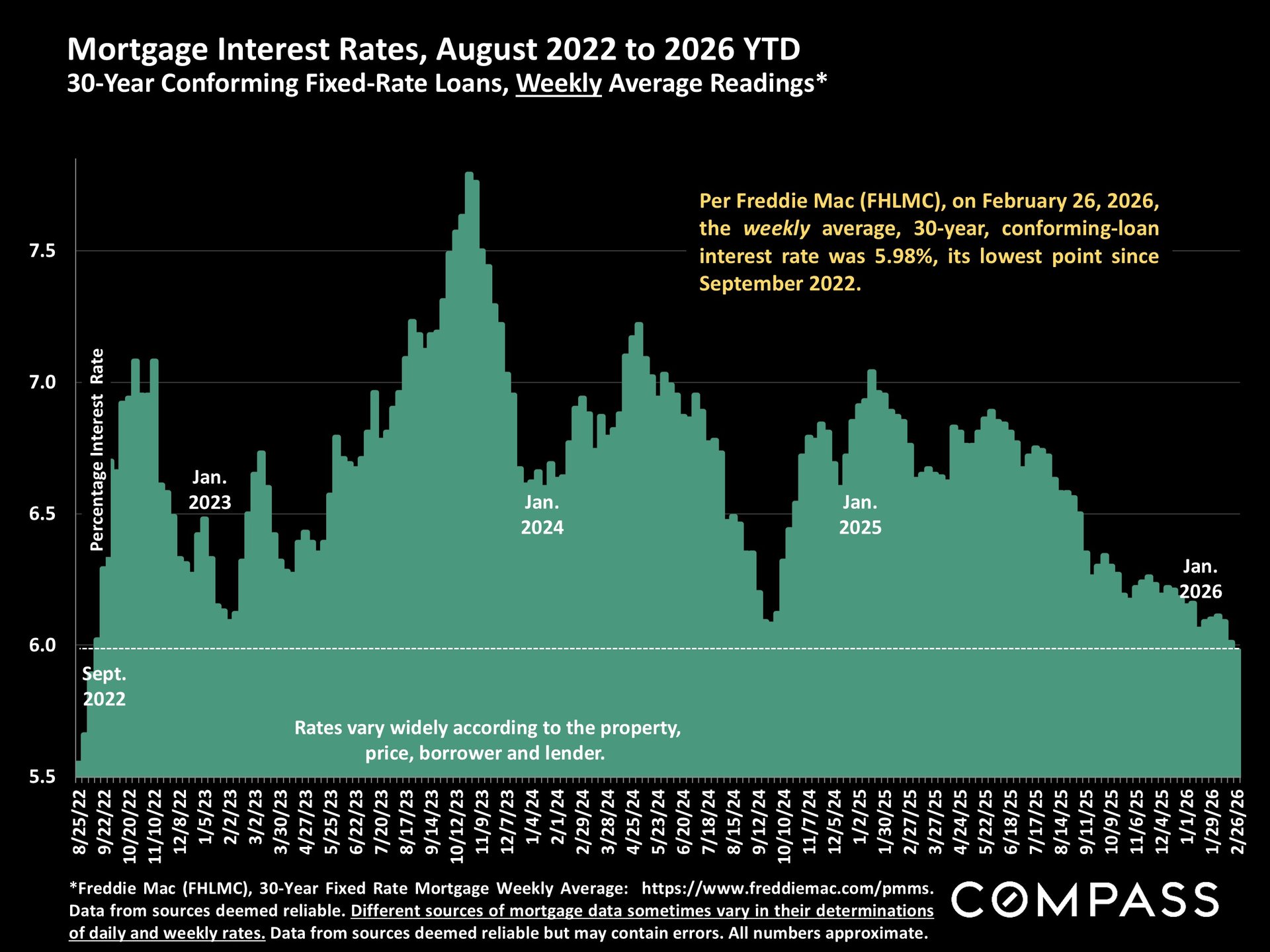

For the first time since September 2022, the weekly average 30-year conforming mortgage rate has fallen below 6 — landing at 5.98% per Freddie Mac’s latest PMMS reading. In a market where borrowing costs have hovered above 7% for much of the past two years, that’s a meaningful shift.

“This rate movement is real, and it matters. We’ve had clients on the sidelines waiting for exactly this kind of signal. At the same time, the broader economic picture is more complicated than one headline — and sophisticated buyers need to understand the full context.

Here’s a thorough look at the economic indicators shaping the landscape for San Francisco luxury buyers right now, drawn from Compass Chief Market Analyst Patrick Carlisle’s latest report.

At 5.98%, the 30-year conforming rate is now at its lowest point since September 2022 — a genuine improvement in purchasing power for anyone who was priced out during the 7%-plus era. The downward trajectory that began in mid-2024 has continued, and the psychological significance of breaking below 6% shouldn’t be underestimated.

That said, a few things are worth keeping in mind for San Francisco buyers specifically. Most luxury transactions involve jumbo loans, which are not directly tied to the conforming rate benchmark and carry their own pricing dynamics. Rates also vary considerably by property type, loan structure, borrower profile, and lender. The headline number is a directional signal, not a quote.

“I always tell clients: the rate you read in the headlines is a starting point, not a finish line. For a South Beach penthouse or a Pacific Heights condo, we’re working in jumbo territory. But directional movement matters, and right now the direction is right.”

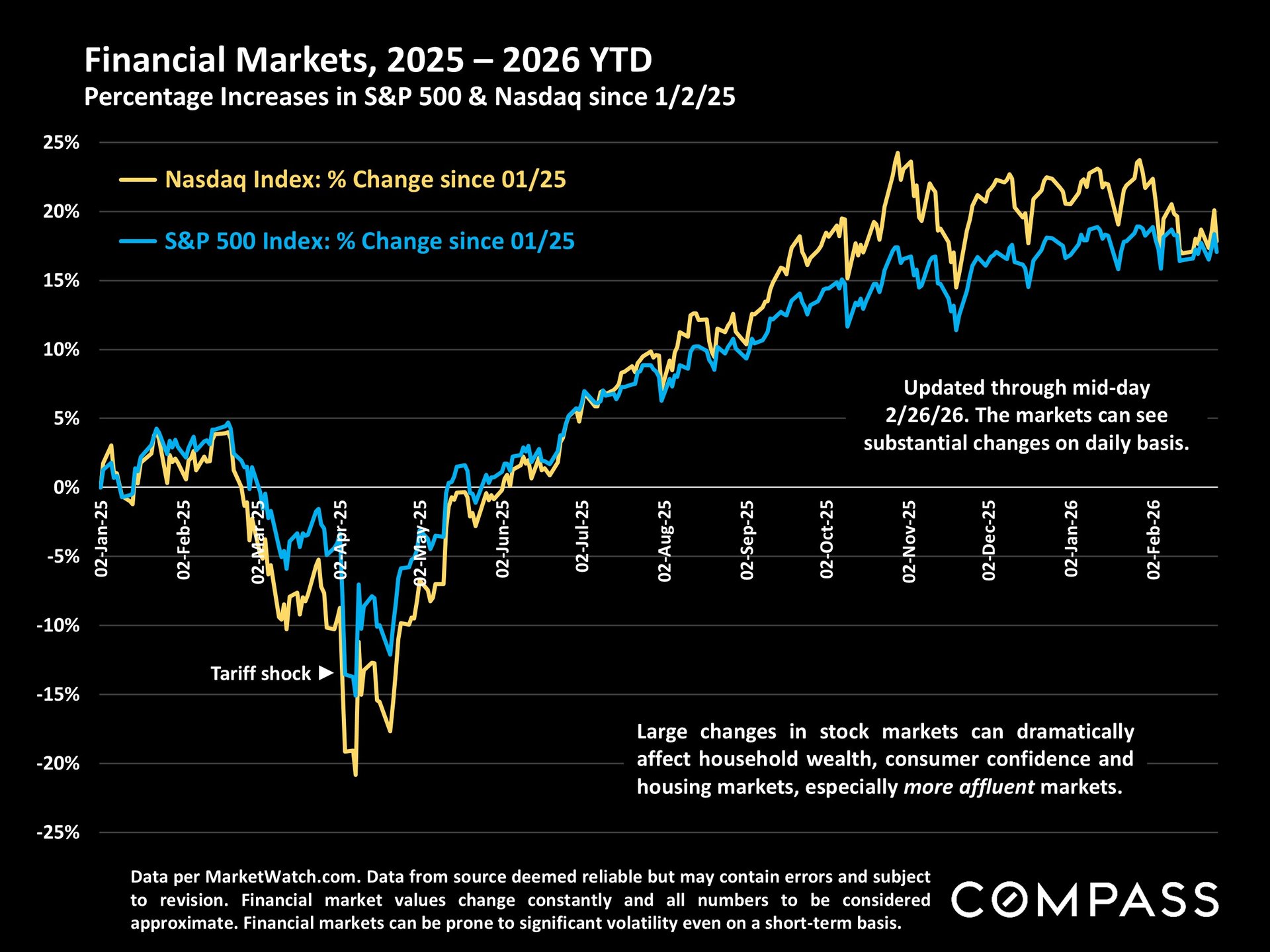

On a year-to-date basis since January 2025, both the Nasdaq and S&P 500 have posted solid gains. But the path has been bumpy. A significant tariff shock rattled markets mid-year, and more recently, AI-related fears have put sharp pressure on software, financial services, logistics, professional services, and real estate-adjacent sectors — precisely the industries where many of San Francisco’s luxury buyers work and hold equity.

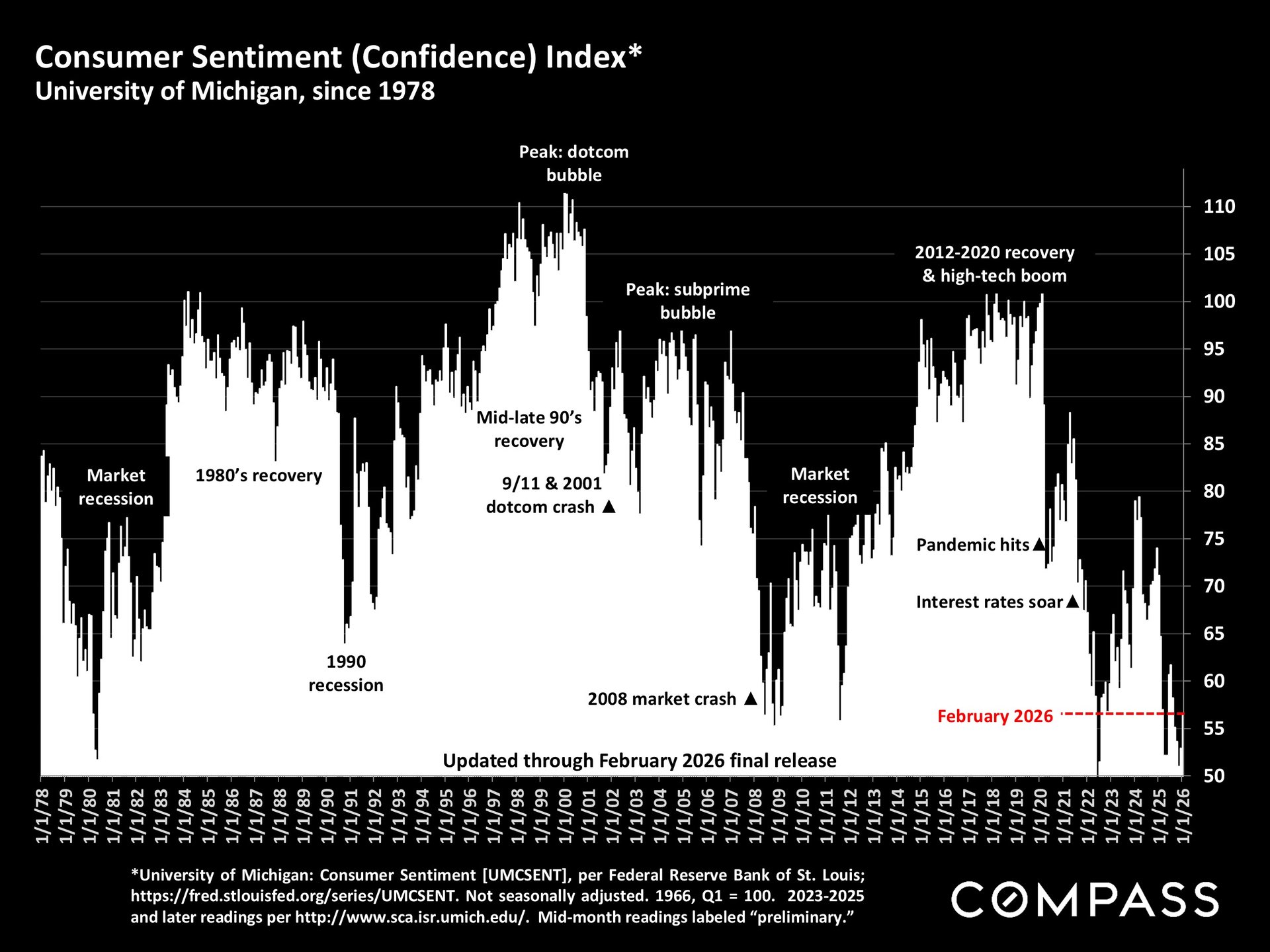

Large swings in portfolio values affect luxury home purchases in two ways: practically, in terms of available liquidity for down payments or all-cash closings; and psychologically, in terms of buyer confidence. The University of Michigan’s Consumer Sentiment Index captures this well — overall sentiment has stagnated, sitting roughly 13% below where it was a year ago. But the data tells a more nuanced story.

Higher-income and college-educated households have actually seen sentiment improve, while lower-income consumers have not. The index notes that wealthier consumers — with stronger income prospects and investment portfolios — feel considerably more insulated from broader economic risk.

“San Francisco’s luxury buyer base is disproportionately in that insulated category. That doesn’t mean volatility is irrelevant — it absolutely is. But our buyers are generally in a stronger position than the headline numbers suggest.

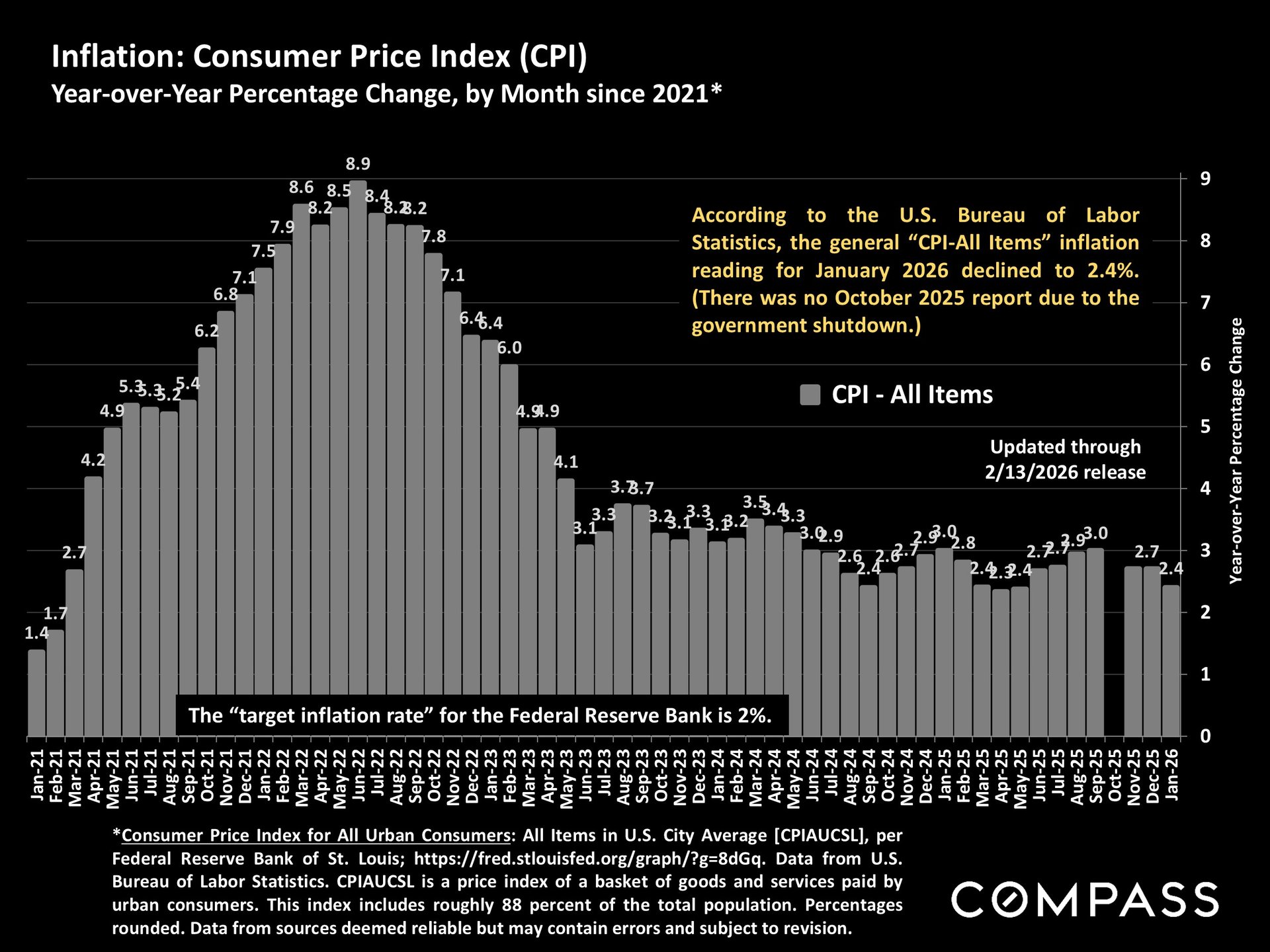

The January 2026 CPI reading came in at 2.4% year-over-year — notably close to the Federal Reserve’s 2% target. (There was no October 2025 report due to the government shutdown.) Housing, insurance, utilities, transportation, and food remain substantially more expensive than their pre-pandemic baselines, but the rate of increase has clearly slowed.

For the Fed, this matters enormously. Continued progress toward the 2% target increases the likelihood of further rate reductions, which flows downstream into mortgage rates. For buyers, a stable inflationary environment simply makes it easier to commit to a major purchase — particularly after years of watching costs move unpredictably in every direction.

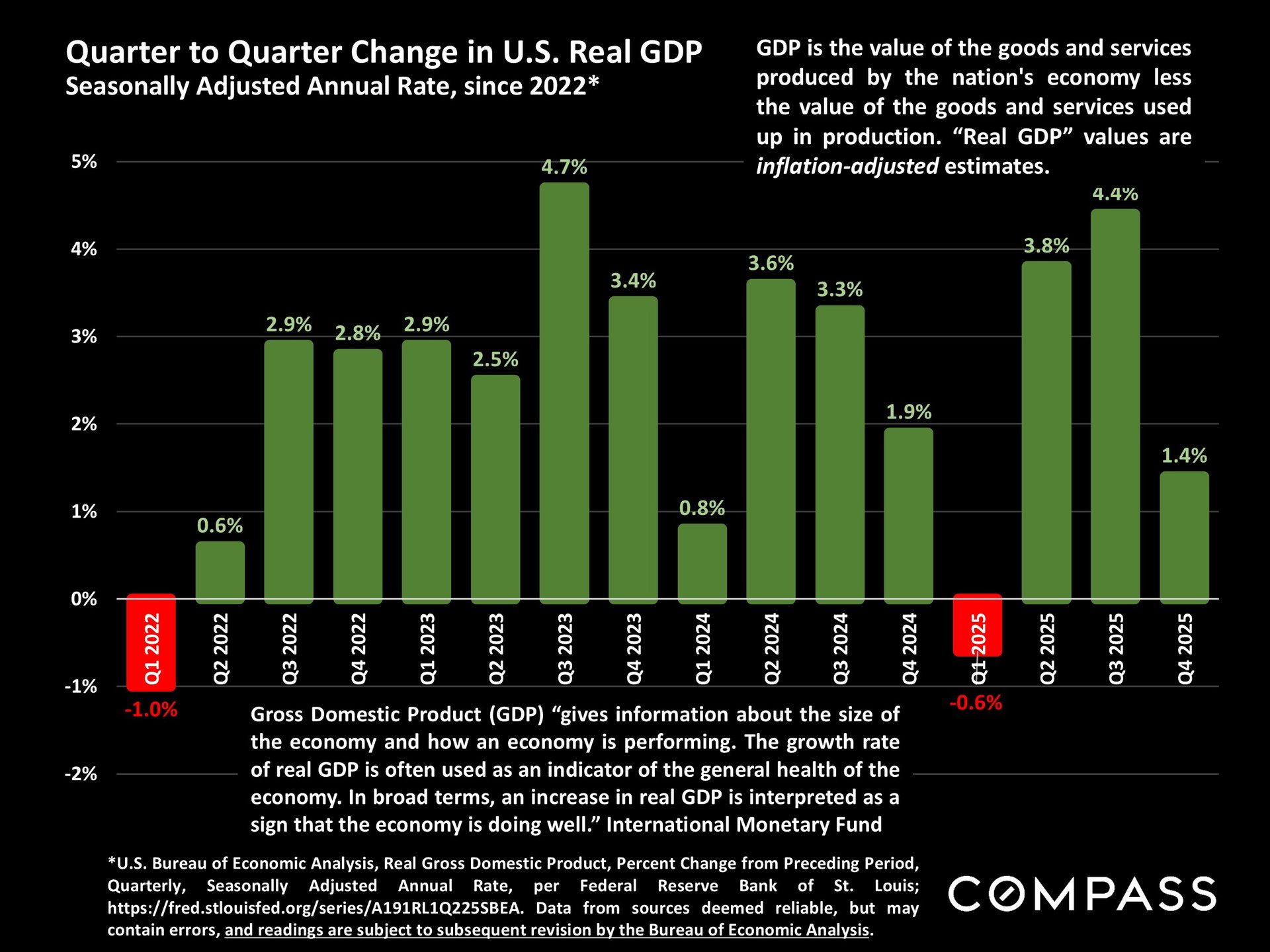

Q4 GDP dropped sharply, per the Bureau of Economic Analysis. The president’s administration attributed the decline largely to the federal government shutdown, though economists continue to debate how much of the contraction that explains.

Prior quarters were solid: Q3 2025 came in at 1.4%, following stronger readings throughout 2024. The Q4 number is a data point to monitor, not a recession signal on its own — but it does add to the broader sense of economic uncertainty that has made buyers in many markets more cautious.

San Francisco’s luxury condo market has historically weathered mild downturns better than the national average, thanks to supply constraints, international buyer interest, and a concentration of high-income professionals in neighborhoods like Yerba Buena, Mission Bay, and Nob Hill.

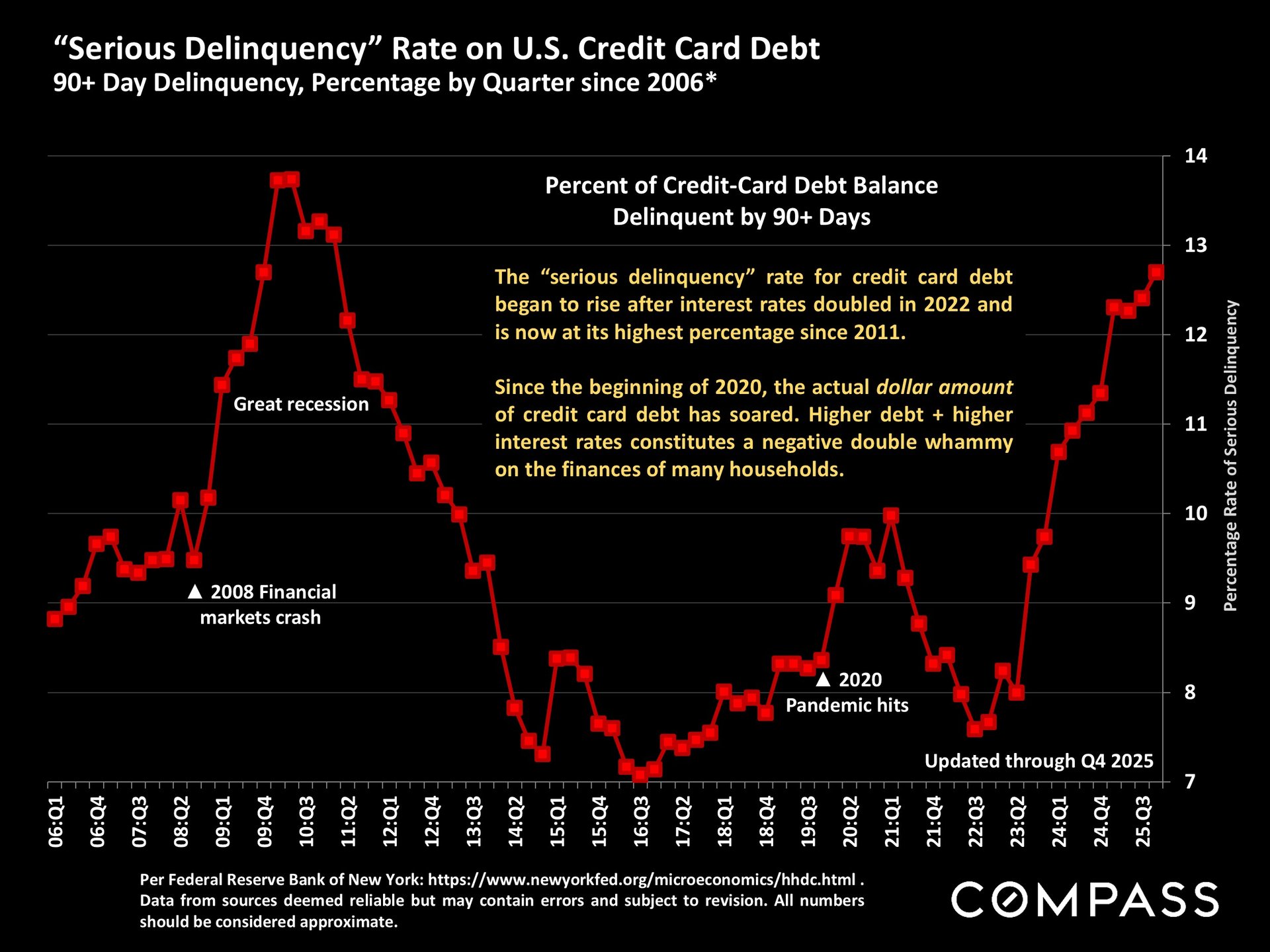

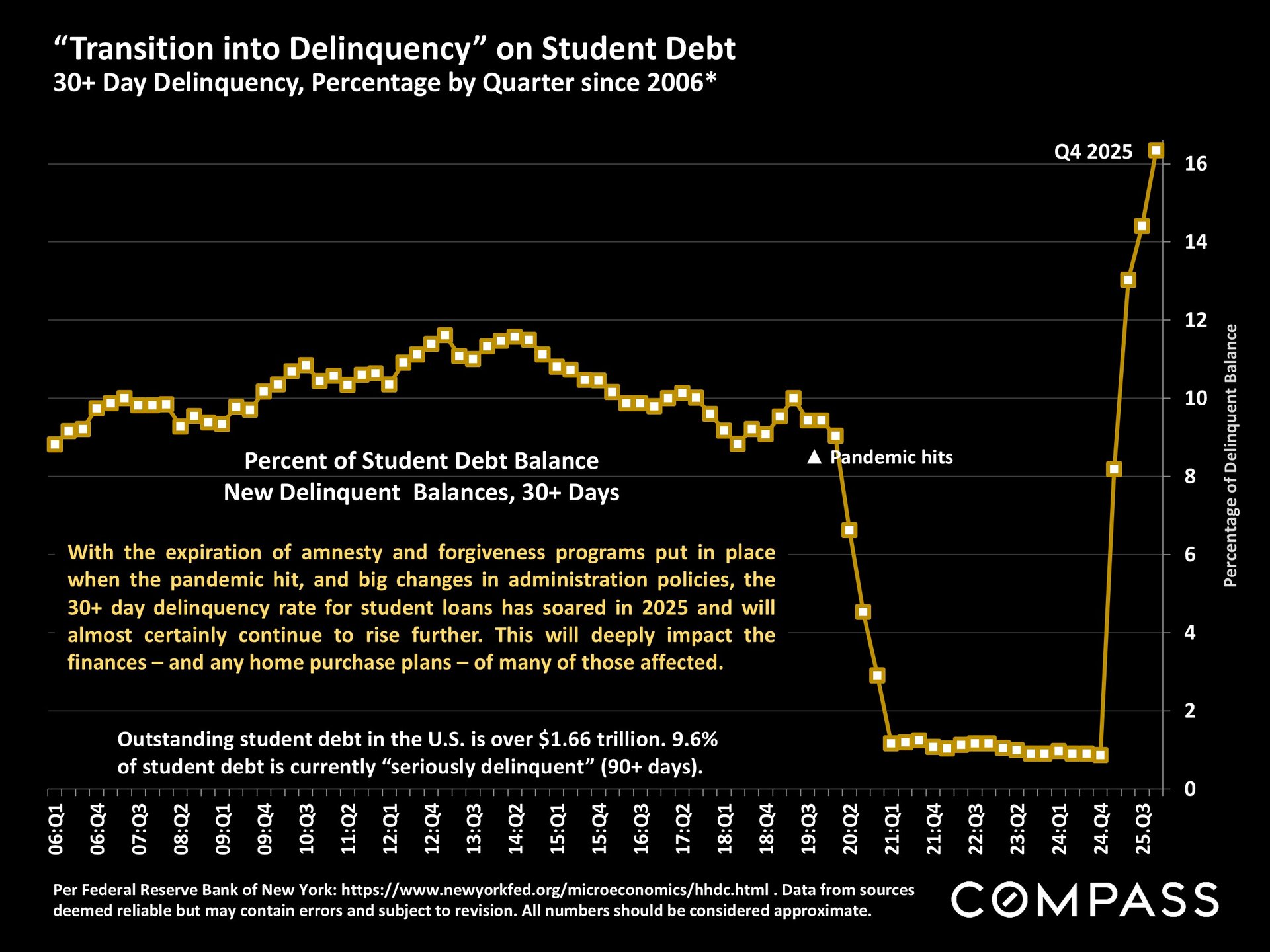

Several debt indicators are flashing yellow in the current economic environment. Understanding them — and who they actually affect — is important context for luxury buyers.

Credit card serious delinquency has reached its highest rate since 2011. Since 2020, both the dollar volume of credit card debt and prevailing interest rates have risen sharply, compounding the burden on lower- and middle-income households. Similarly, student loan delinquency spiked dramatically in 2025 as pandemic-era relief programs expired. With over $1.66 trillion in outstanding student debt nationally, and 9.6% of it now seriously delinquent, this will shape first-time homebuying capacity for years to come.

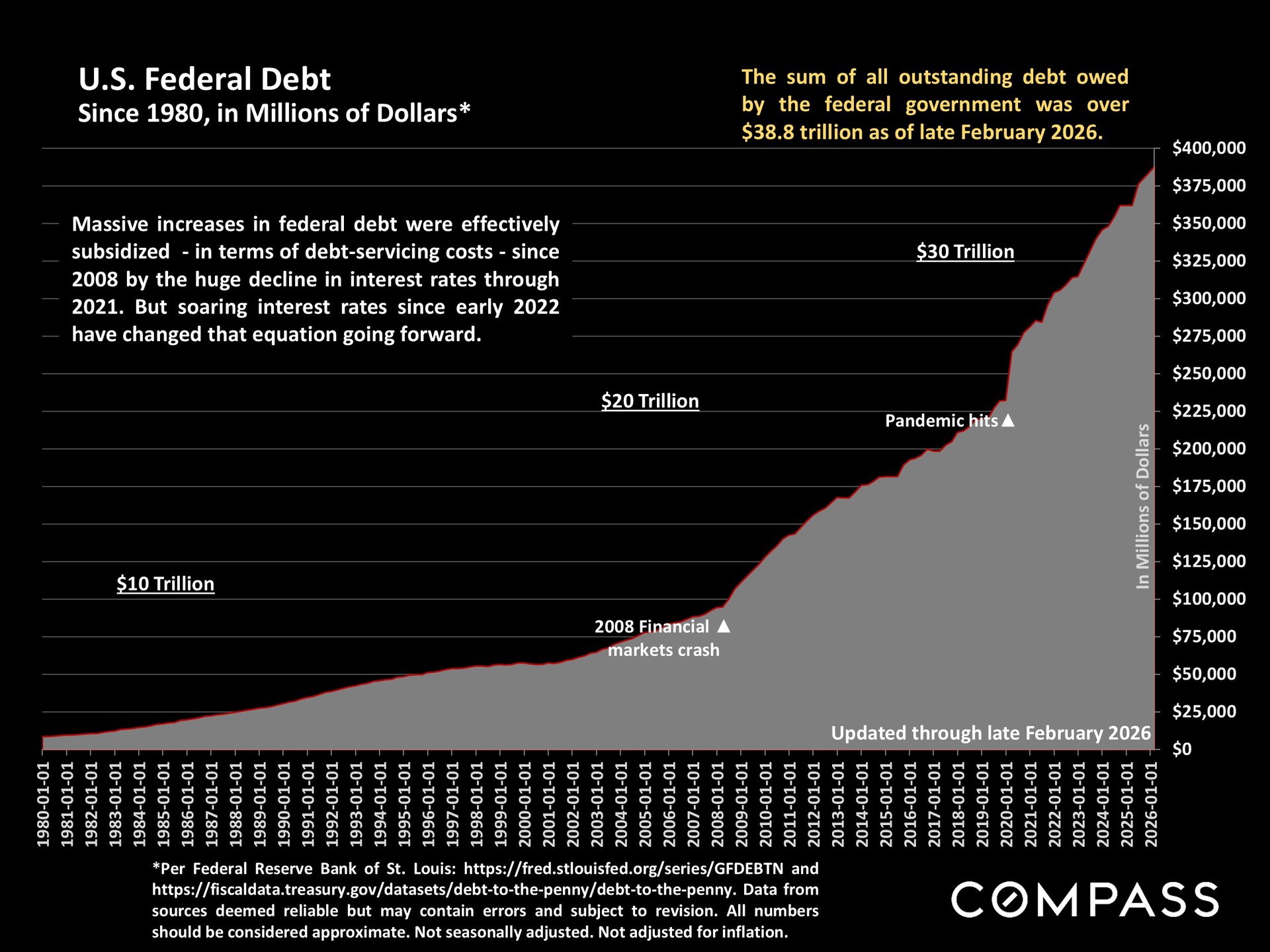

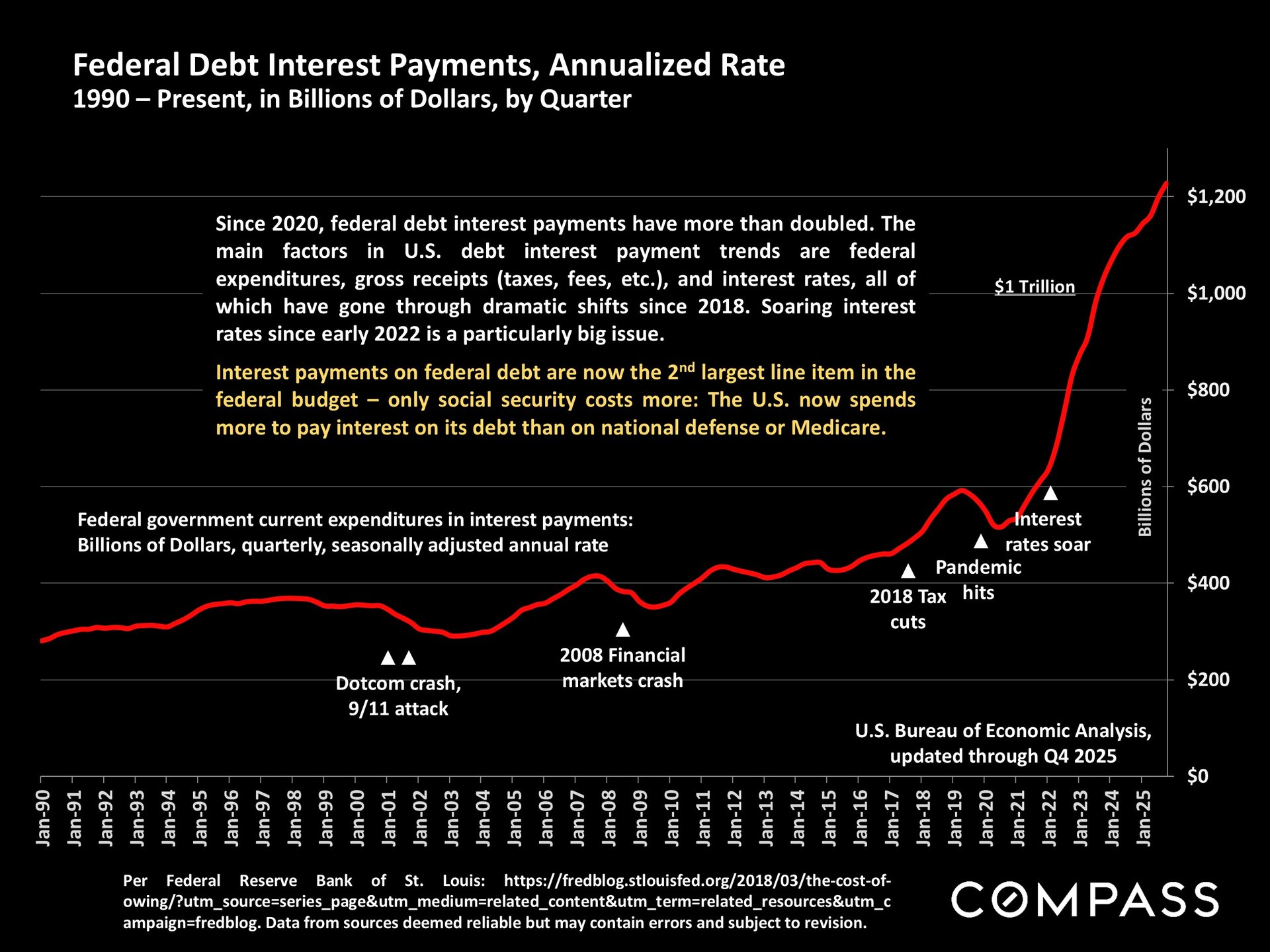

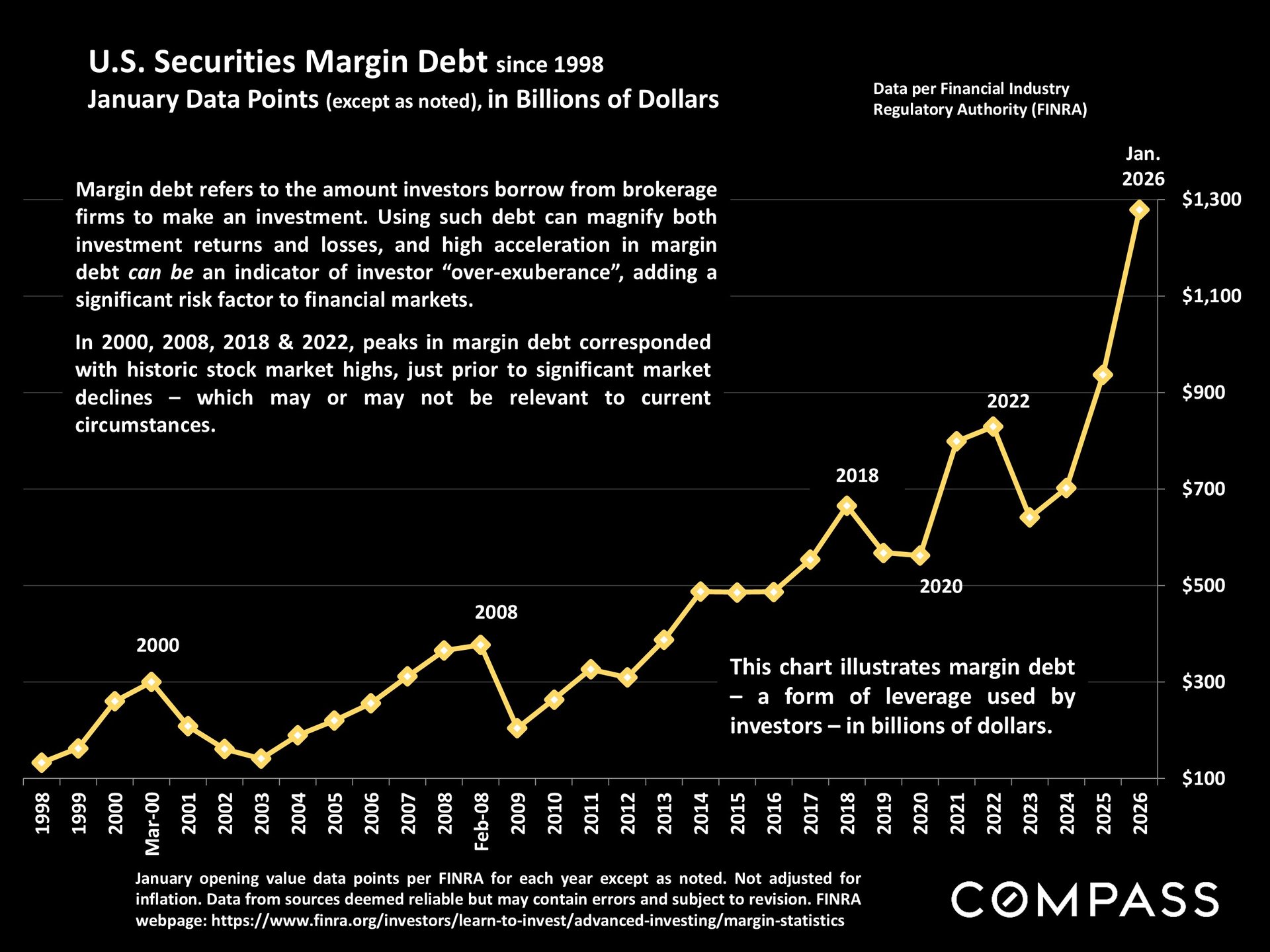

At the macro level, U.S. federal debt has surpassed $38.8 trillion, and annualized interest payments on that debt have exceeded $1 trillion — now the second-largest line item in the federal budget, behind only Social Security. Meanwhile, U.S. securities margin debt hit a new all-time high in January 2026, echoing patterns that preceded market corrections in 2000, 2008, 2018, and 2022 — though past peaks don’t guarantee the same outcome this time.

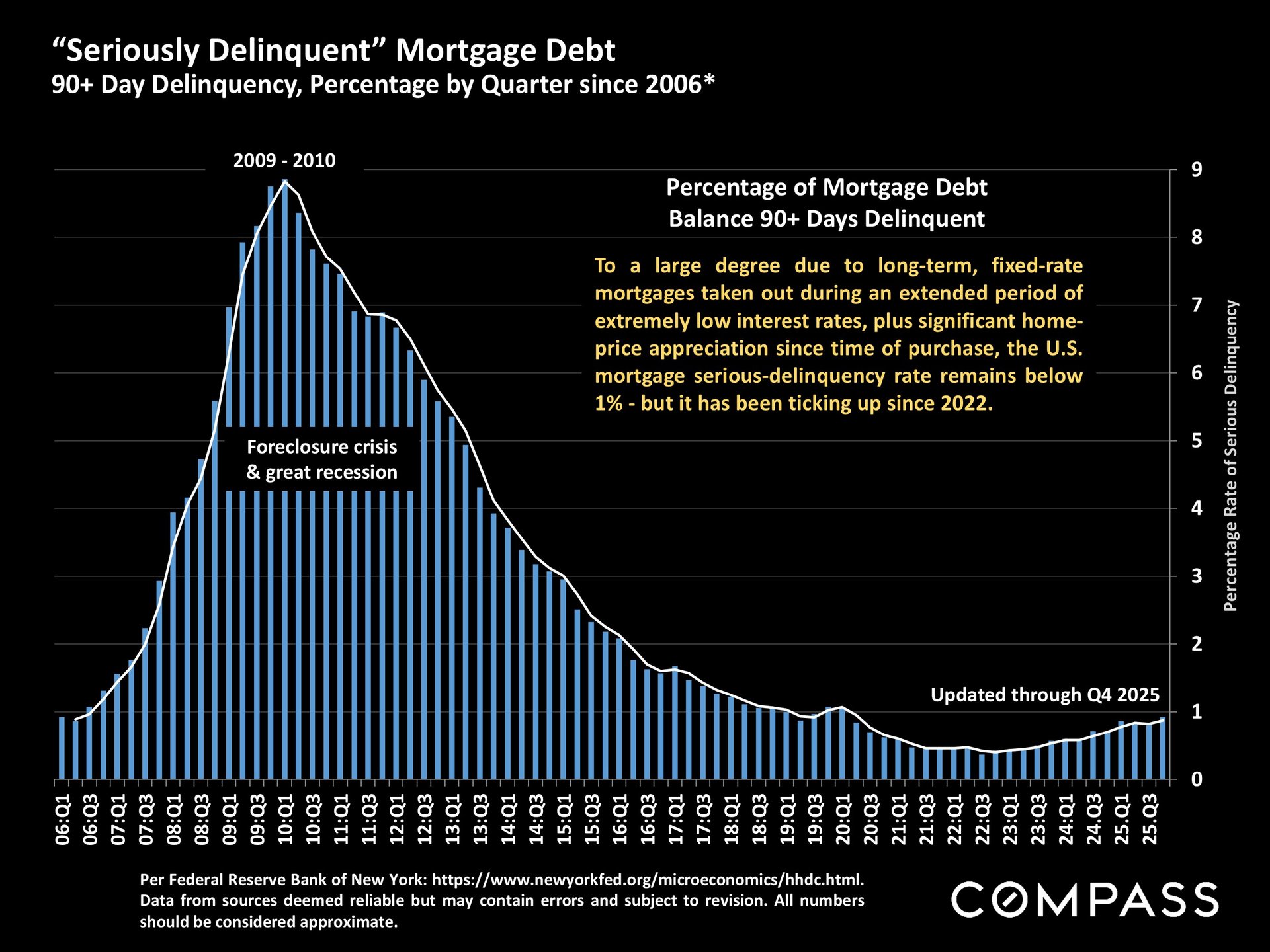

Here’s the important counterpoint: serious mortgage delinquency remains below 1%. Most homeowners — particularly those who locked in fixed rates during 2020–2021 — are not under meaningful payment pressure. And the buyer profile in San Francisco’s luxury market is fundamentally different from the consumers driving credit card and student debt stress.

“The debt picture is nuanced. Consumer debt stress is real at lower income levels. But the homeowning population — and certainly the luxury buyer pool in South Beach, Lower Pacific Heights, or Russian Hill — looks very different from those statistics. Mortgage health is solid, and that matters for market stability.”

The combination of a 3.5-year low in mortgage rates, stabilizing inflation, and a luxury buyer pool that remains largely insulated from broader consumer debt pressures makes for a genuinely interesting moment in the San Francisco market. The macro environment isn’t without risk — stock market volatility, an uncertain GDP outlook, and elevated federal debt all argue for measured decision-making.

For buyers who have been waiting for a clear entry signal, the current rate environment offers one. For sellers, improving affordability and renewed buyer confidence in premium neighborhoods — from Yerba Buena to Pacific Heights to Nob Hill — should support well-priced listings this spring.

If your purchase is tied to equity assets or a stock-compensation event, the current volatility is worth factoring into your timeline and financing structure. But for buyers with stable liquidity, rates near their recent lows and a motivated seller environment create a window that hasn’t been available for several years.

“The data right now is telling a story that favors decisive, well-prepared buyers. The window won’t stay open forever. The clients who act when conditions align — rather than waiting for perfect — tend to look back on these decisions very well.

I am a Global Luxury Specialist with Compass, focused exclusively on San Francisco’s premier high-rise condo and penthouse market, including South Beach, Yerba Buena, Mission Bay, Pacific Heights, and Nob Hill. With 17+ years of experience working with discerning buyers and sellers at the intersection of market data and high-touch client service, I can help you assess exactly where you stand in the current environment.

Call or text: (415) 704-3640

Schedule a consultation: rises.co/contact

Primary phone

(415) 704-3640License Number

#02056250Address

891 Beach St,Sean Mamola is a San Francisco real estate agent who specializes in luxury properties and penthouses throughout the city's most coveted neighborhoods. As a Global Luxury Specialist with Compass and Rises.co, Sean works with discerning clients who are buying and selling exceptional properties in San Francisco. Since 2018 he has closed 75+ transactions and more than $100M in sales volume across the city's high-rise condo and penthouse market.

Sean focuses on San Francisco's premier areas including South Beach, Yerba Buena, Mission Bay, Pacific Heights, Lower Pacific Heights, Russian Hill, and Nob Hill. His deep knowledge of these neighborhoods allows him to guide clients to properties that perfectly match their lifestyle and investment goals.

Whether you're drawn to the modern luxury of South Beach condos, the urban sophistication of Yerba Buena, the waterfront appeal of Mission Bay, the timeless elegance of Pacific Heights, the historic charm of Russian Hill, or the prestigious heights of Nob Hill, Sean understands what makes each area unique.

For Sellers

Sean creates comprehensive marketing strategies that attract qualified buyers with refined tastes. He believes in elegant staging with meticulous attention to detail, ensuring your property makes an unforgettable impression. His marketing reaches both international and local luxury markets, maximizing exposure for condos, penthouses, condotels, and new developments.

For Buyers

Using cutting-edge technology and market research, Sean carefully analyzes pricing and property trends to find homes that satisfy his clients' specific preferences, price points, and lifestyles. His 24/7 availability and white-glove service ensure you never miss the right opportunity.

Working with Sean and his partnership with Rises.co gives clients significant competitive advantages. His vast network of interconnected agents results in winning offers and an impressively low ratio of properties shown to offers accepted. Sean's impeccable work ethic and precise negotiation skills ensure sellers find the right buyer and buyers secure their dream home.

Before becoming a licensed real estate agent, Sean spent years in luxury hospitality, skills he applies to every client relationship and transaction. He has tremendous respect for people's privacy and consistently exceeds expectations – from international travel to execute transactions to handling unique special requests.

As a Bay Area native who lived in New York City for 15 years, Sean brings a global perspective and genuine appreciation for people from all walks of life. His diverse background helps him connect with clients whether they're local San Francisco residents or international buyers seeking their perfect property.

When not working, Sean enjoys cycling, spending time with his large Irish-Italian family, and volunteering for Food Runners, The Richmond/Ermet Aid Foundation (REAF), and Broadway Cares/Equity Fights AIDS. This community involvement reflects his commitment to giving back to the city he serves.

If you're looking for an exceptional San Francisco real estate agent who specializes in luxury properties and provides truly high-touch service, let's talk. Sean is ready to help you find your perfect San Francisco home or achieve the best possible outcome when selling your property.

Specializing in luxury condos, penthouses, and exceptional properties in South Beach, Yerba Buena, Mission Bay, Pacific Heights, Lower Pacific Heights, Russian Hill, and Nob Hill.

Stay up to date on the latest real estate trends.

Sean Mamola | July 29, 2026

How Fillmore and Japantown condos are selling in 2026, for sellers.

Sean Mamola | July 28, 2026

Central, cultural, and mid-value: Fillmore and Japantown condos in 2026.

Sean Mamola | July 27, 2026

Deciding whether to sell or lease your Mission Bay condo? Compare market demand, HOA rules, taxes, and local costs to choose wisely.

Sean Mamola | July 26, 2026

Compare Mission Bay and SOMA condos for first-time buyers in San Francisco, from pricing and transit to lifestyle and inventory.

Sean Mamola | July 24, 2026

How Lower Pacific Heights condos are selling in 2026, for sellers.

Sean Mamola | July 23, 2026

What buyers should know about Lower Pacific Heights condos in 2026.

Sean Mamola | July 22, 2026

How Van Ness / Civic Center condos are selling in 2026, for sellers.

Sean Mamola | July 21, 2026

San Francisco's central value high-rise corridor, decoded for 2026 buyers.

Sean Mamola | July 16, 2026

When a condo loan stalls, it is usually the building, not the borrower. Here is how to get ahead of it.

CONTACT SEAN MAMOLA AT RISES.CO

CA DRE# 02056250

891 Beach St.,

San Francisco CA 94109