Inside the San Francisco Housing Market Surge in 2026

Sean Mamola | February 12, 2026

Sean Mamola | February 12, 2026

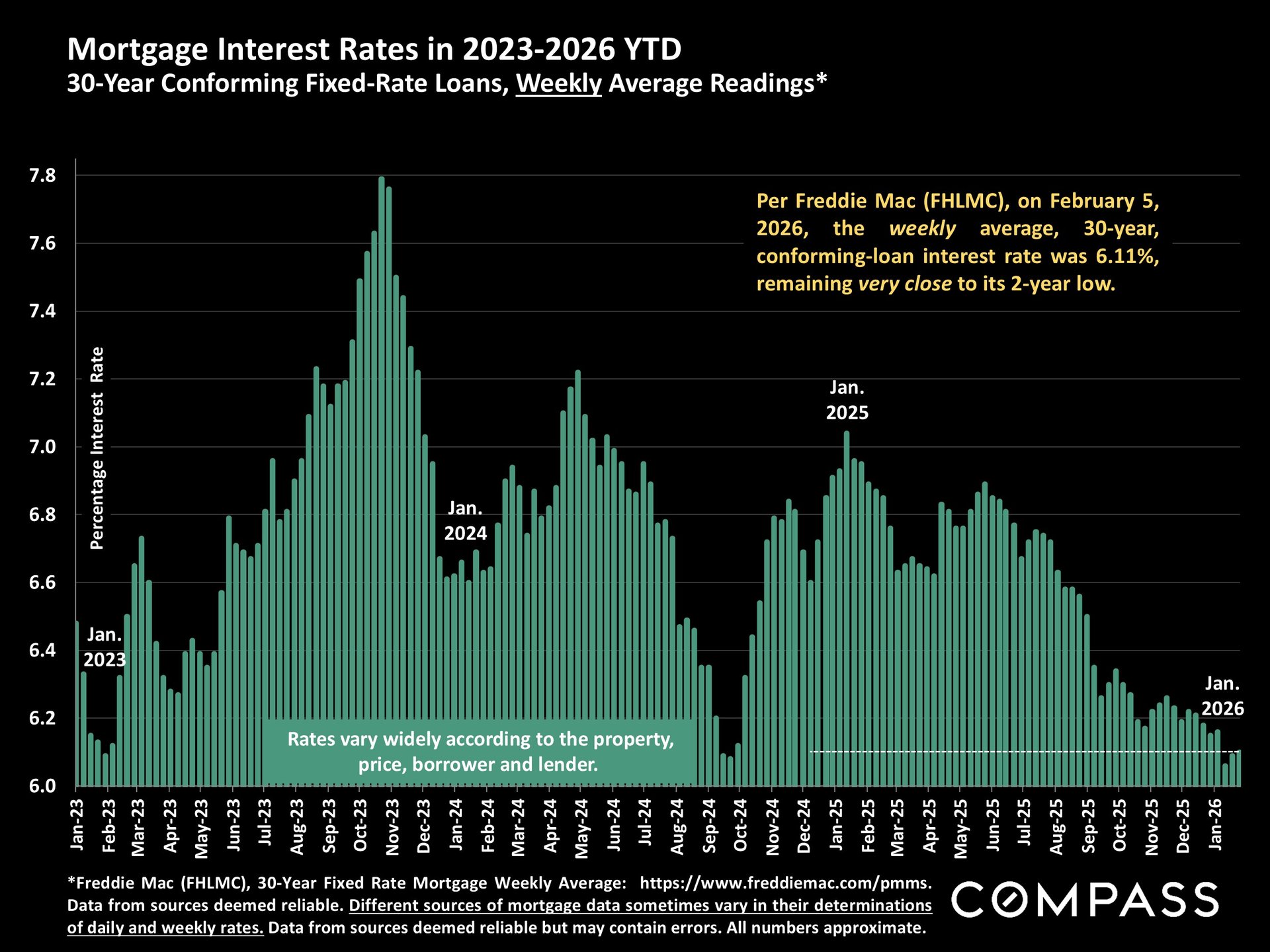

If you’ve been following national real estate coverage, the picture looks cautious but stable. Home prices across the country are barely moving—Redfin’s latest data shows the median U.S. home-sale price up just 1% year over year. Pending sales have been mixed, inventory growth is slowing down, and buyers in many markets still have time to negotiate. Mortgage rates are hovering near 6.11%—close to a 2-year low per Freddie Mac—gently nudging demand higher across the country.

The national story is ‘buyers still have leverage.’ The San Francisco story is ‘if you see something you like, move fast.’ The gap between national headlines and local reality has never been wider.

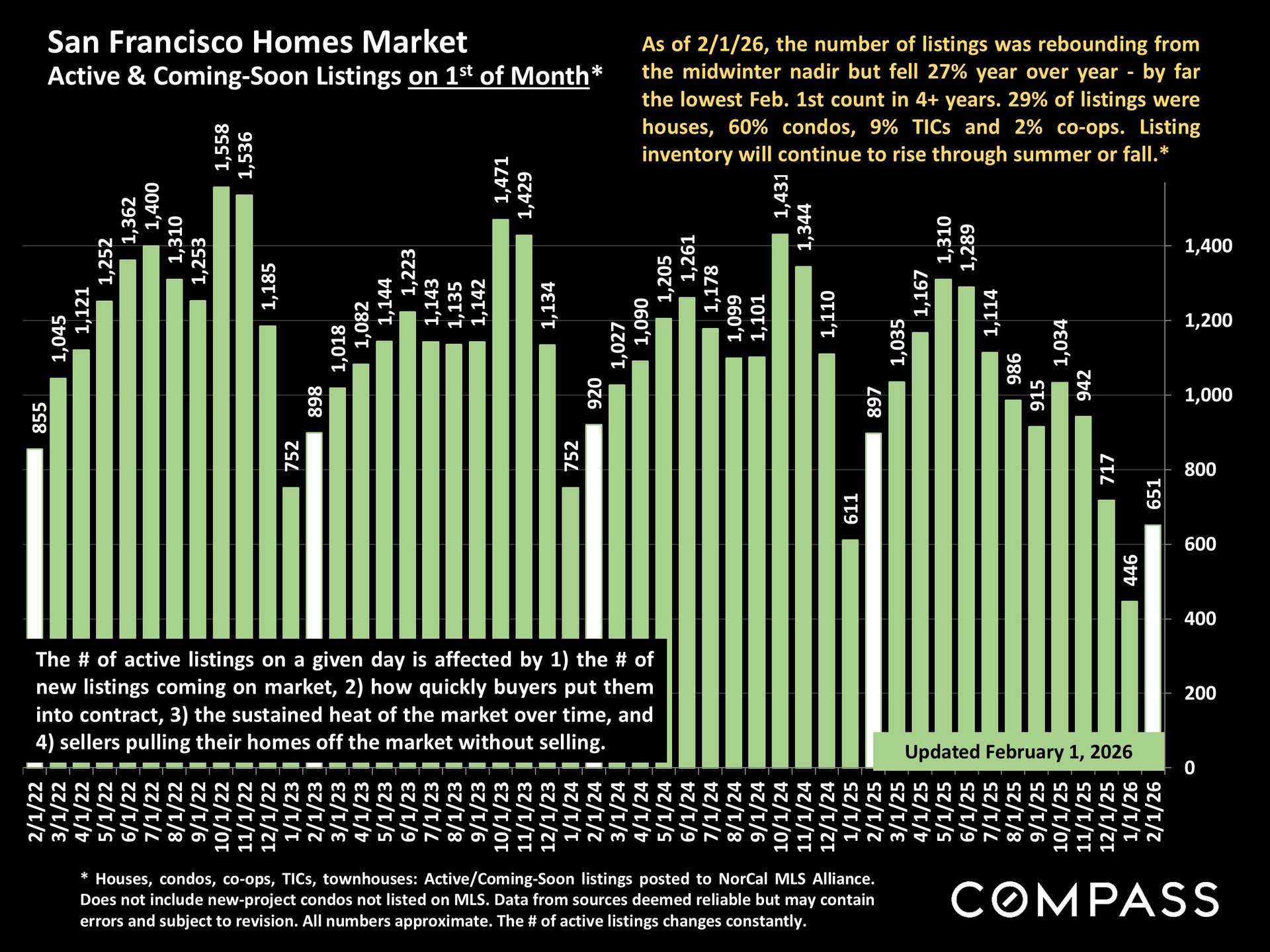

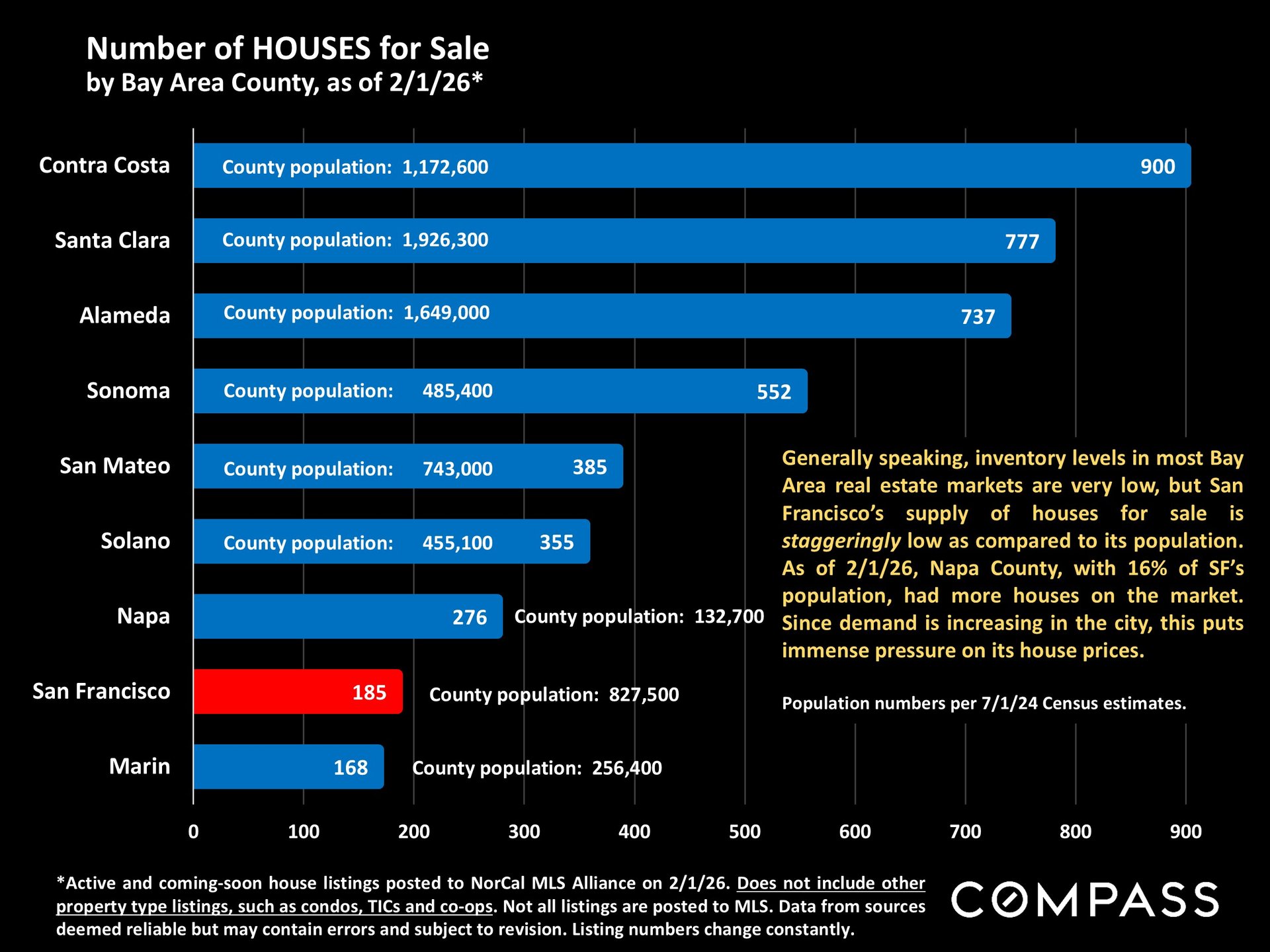

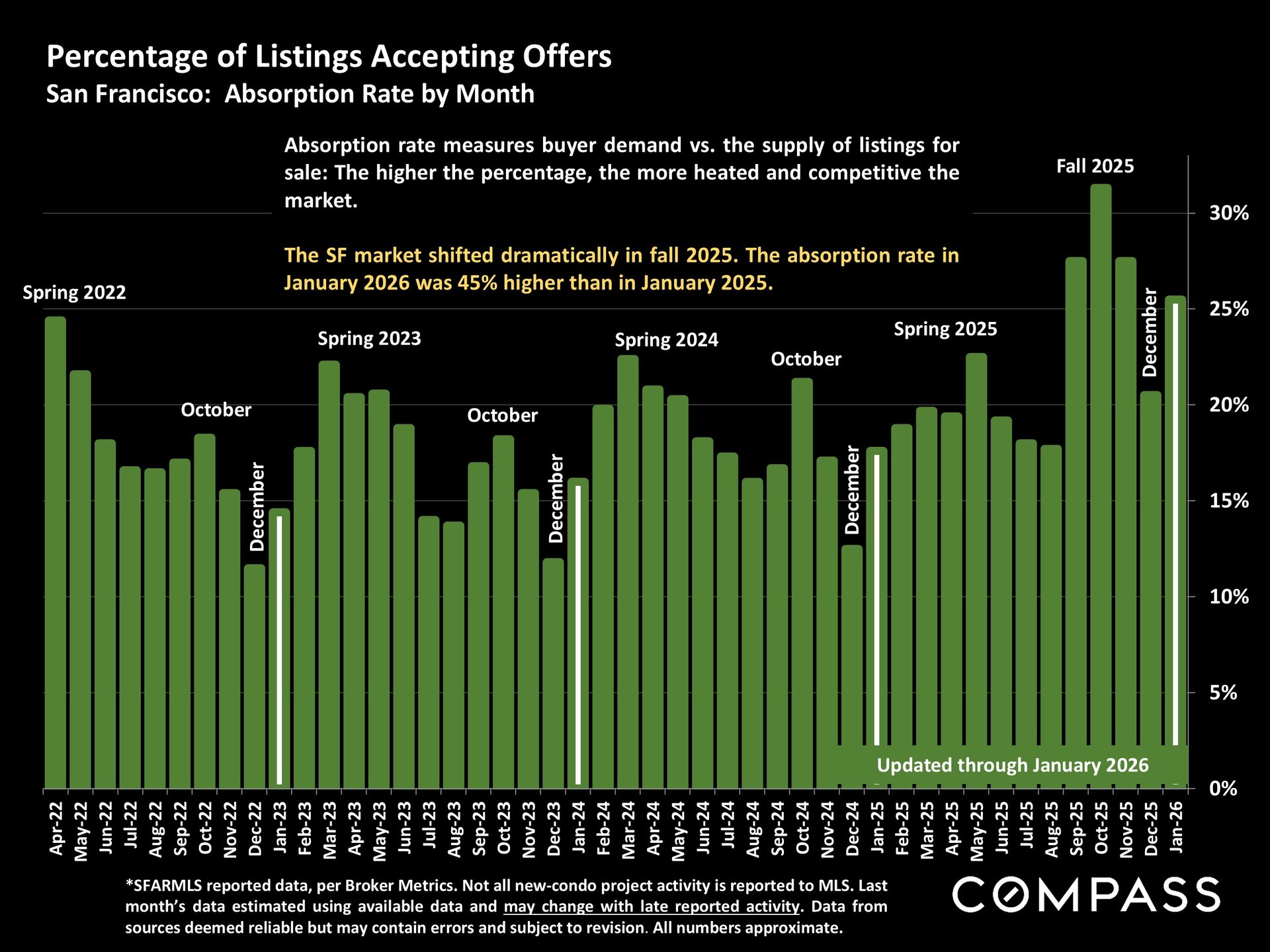

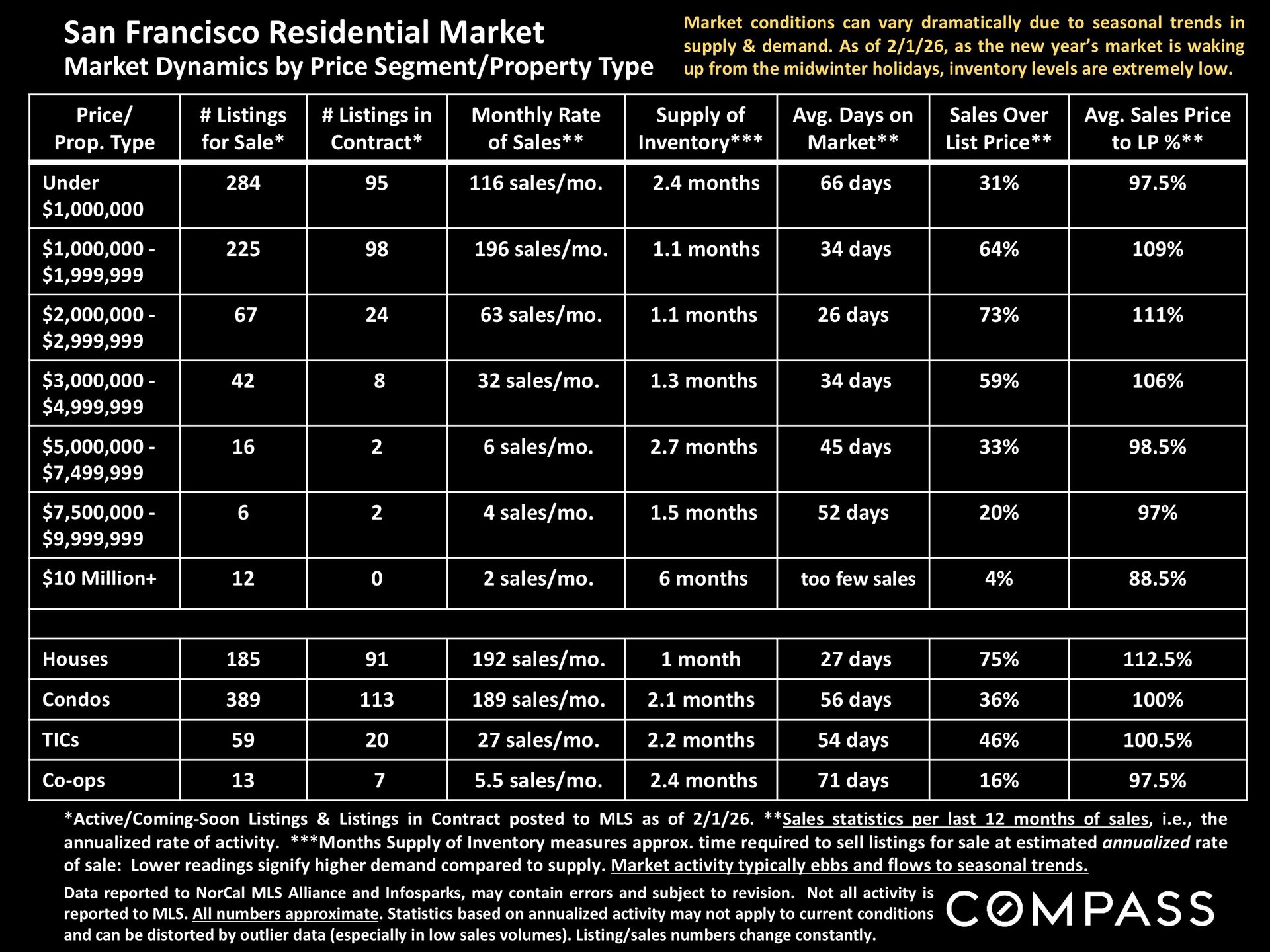

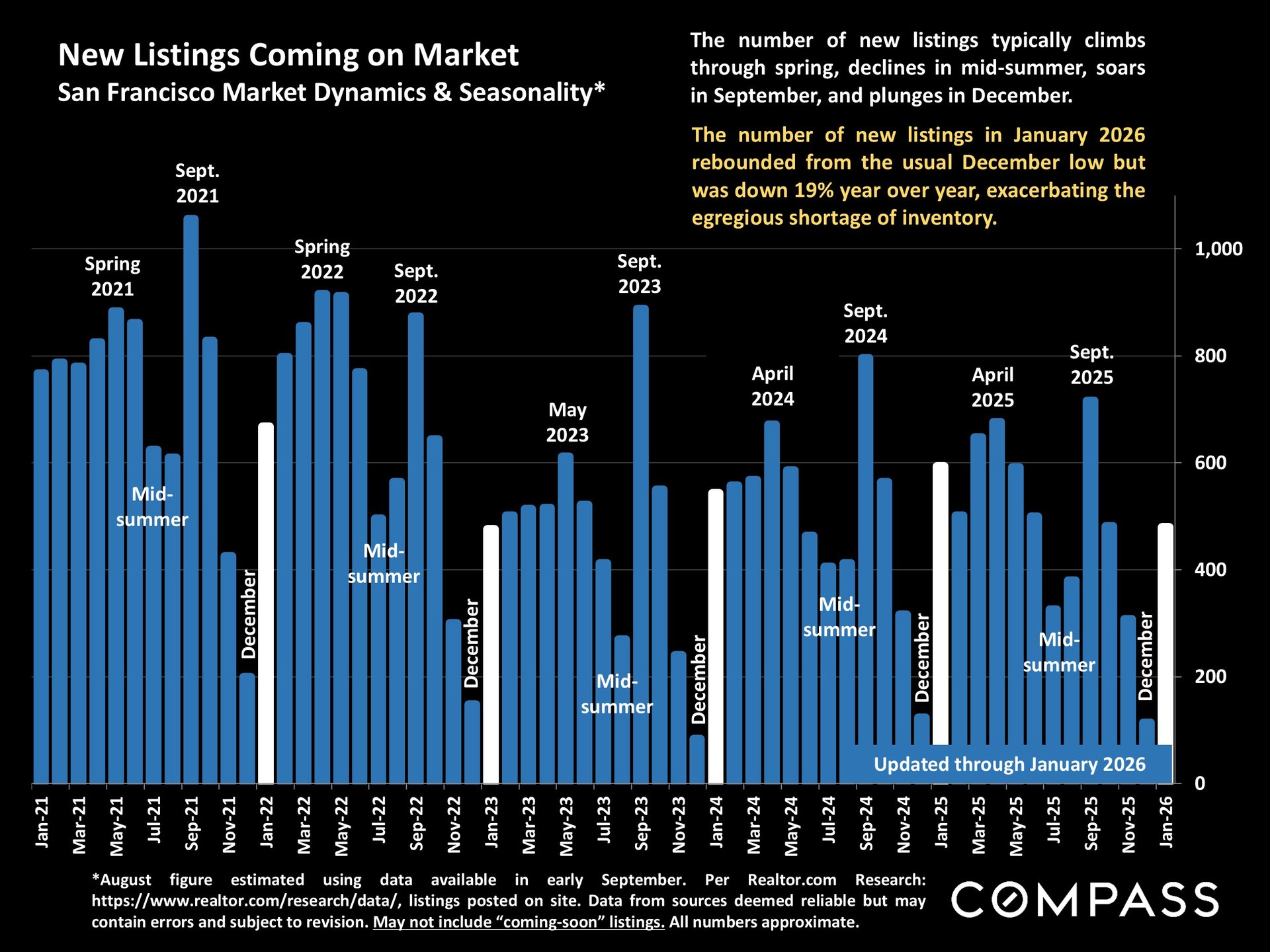

While much of the country debates whether spring will bring a surge of new supply, San Francisco’s inventory just hit its lowest February count in over four years. As of February 1st, just 651 homes were on the market—down 27% from a year ago. To put that number in context, only 185 of those are houses. Napa County, with roughly 16% of San Francisco’s population, currently has more houses listed for sale.

The supply shortage is getting worse, not better. New listings coming on the market in January were down 19% year over year, meaning the already tight pipeline is tightening further. For buyers in neighborhoods like South Beach, Yerba Buena, Mission Bay, and Pacific Heights, this translates directly into faster sales and more competitive offers.

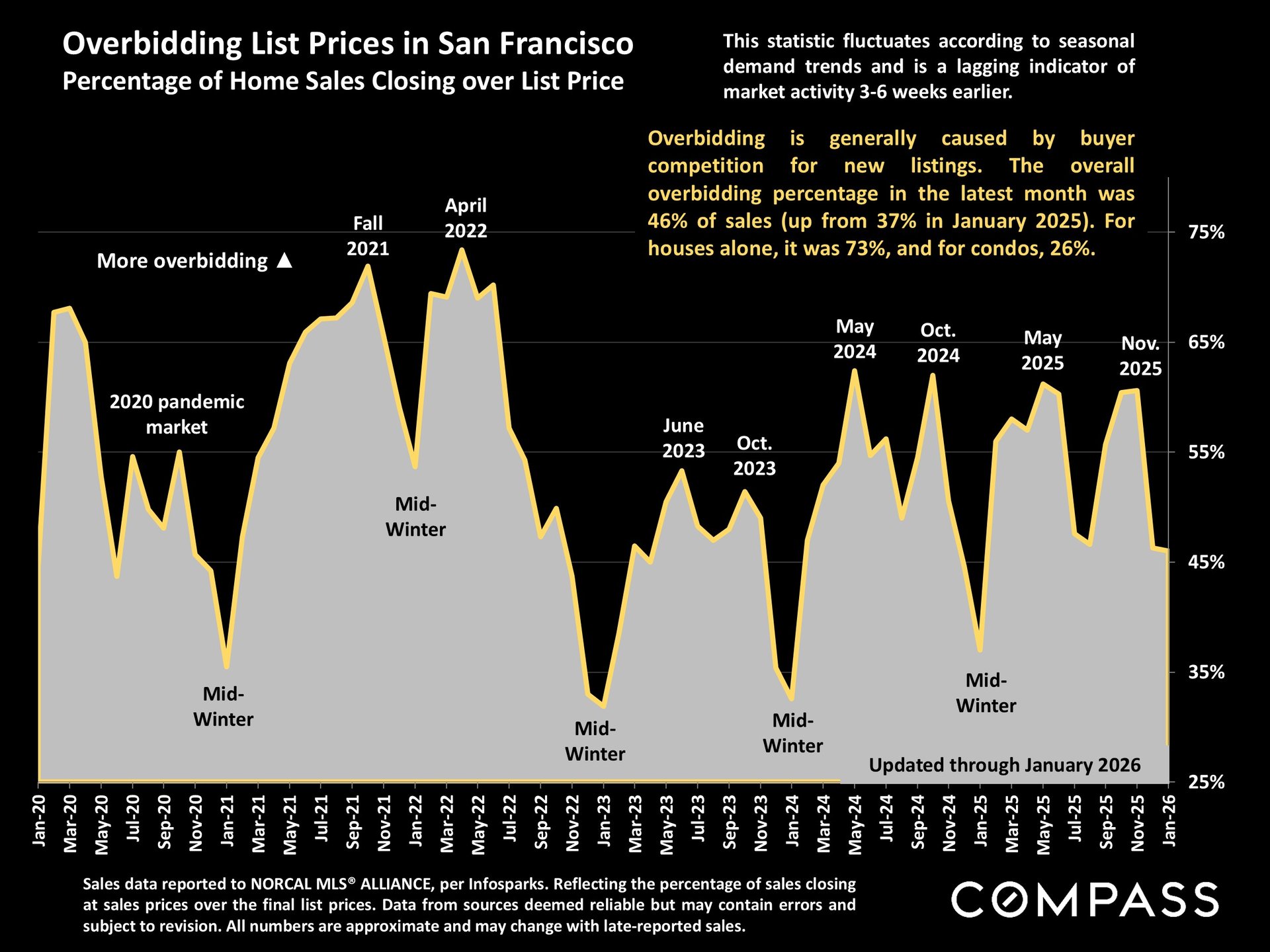

The demand indicators are equally striking. The absorption rate in January—which measures buyer demand relative to the supply of available listings—was 45% higher than January 2025. Price reductions dropped 33% year over year, a clear sign that sellers are pricing with confidence and buyers are meeting them there (or above). And 46% of all sales closed over asking price, up from 37% a year ago.

For houses specifically, the numbers are even more dramatic. Fully 75% of house sales closed over asking, with an average sale price landing at 112.5% of list price. Houses are averaging just 27 days on market. In a city where only 185 houses are available to buy, that kind of competition was inevitable.

“One number that really jumped out this month: in the $2M–$3M range, 73% of sales closed over asking with an average of just 26 days on market. That’s the sweet spot of SF real estate, and it’s moving fast.

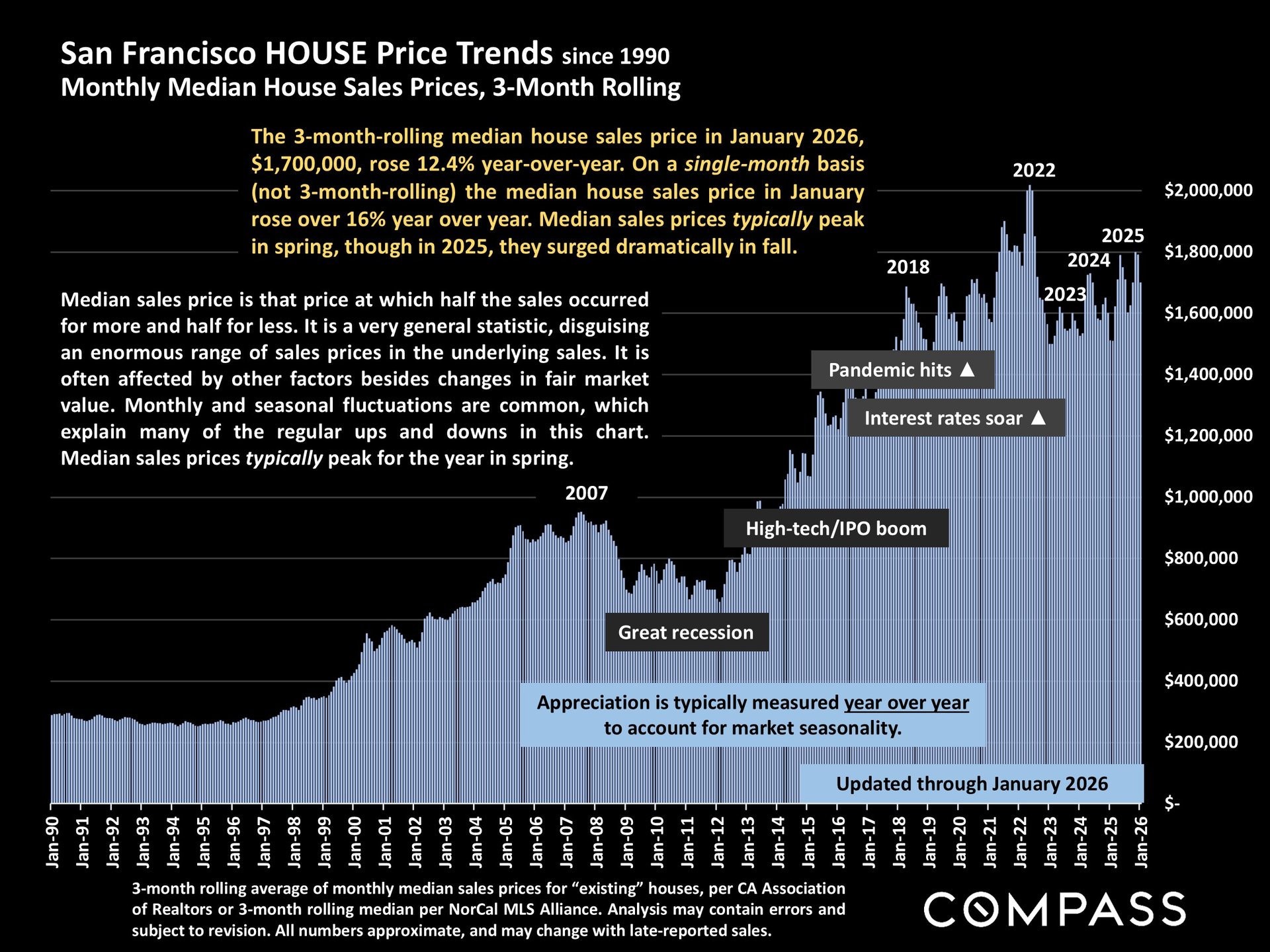

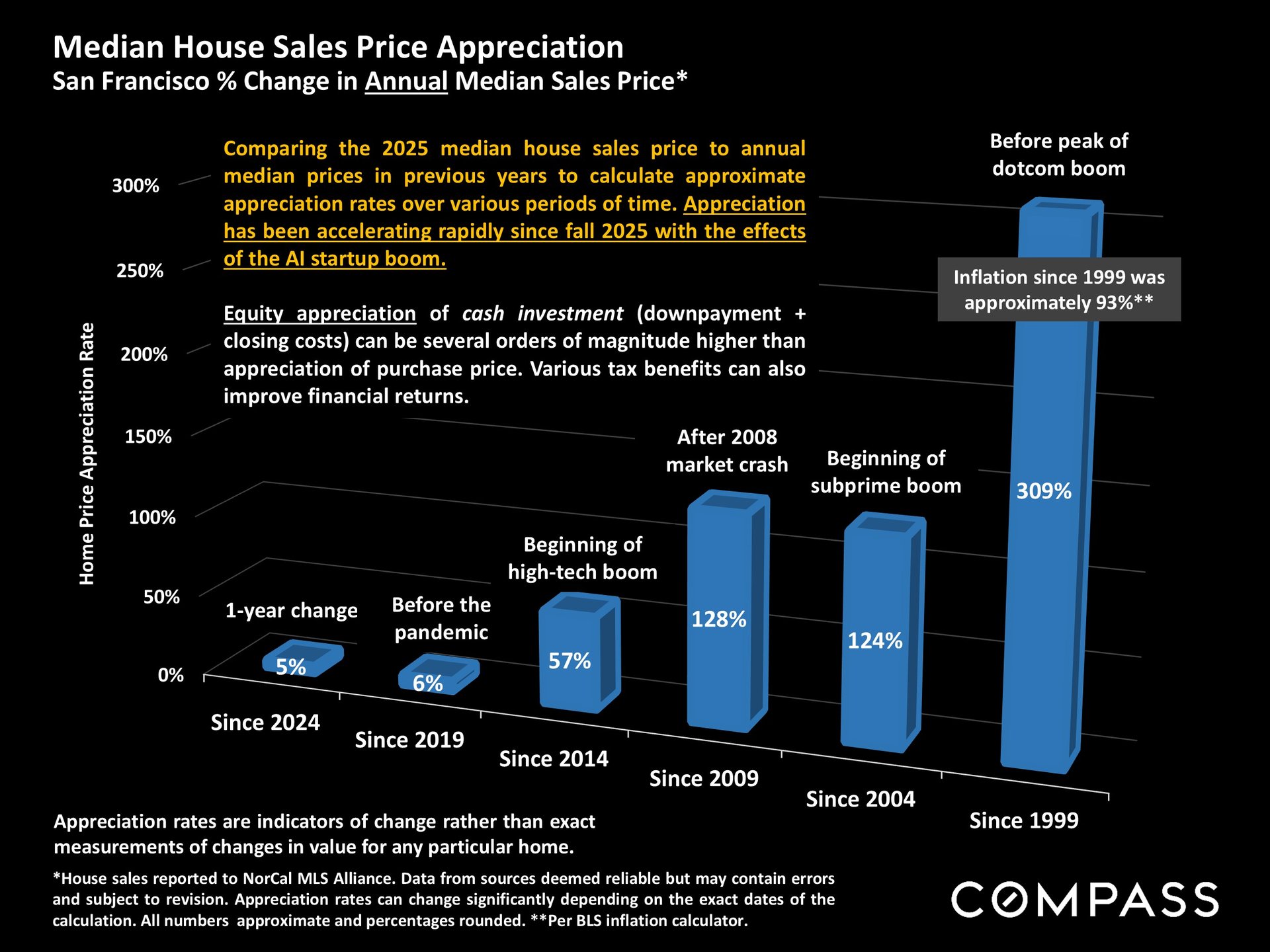

The 3-month rolling median house sales price hit $1.7 million in January 2026, up 12.4% year over year. On a single-month basis—stripping away the smoothing effect of a rolling average—the median house price surged over 16%. That’s a different planet from the national picture, where prices are inching up roughly 1%.

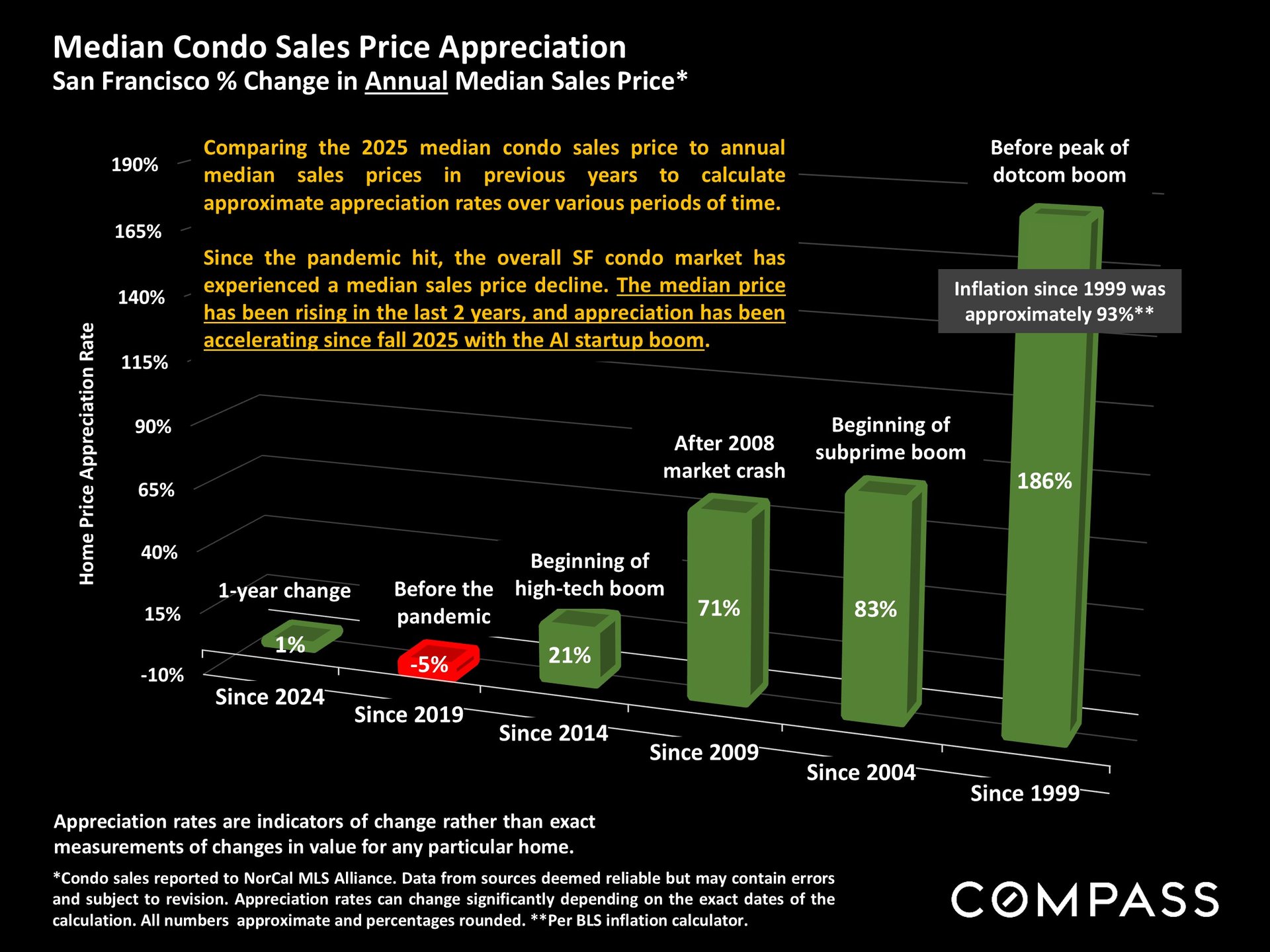

Looking at longer time horizons, the appreciation story is equally compelling. Compared to 2019—before the pandemic—the median house price is up about 6%. Since 2014, it’s risen 57%. Since 2009, following the financial crisis, the increase is approximately 128%. These aren’t just abstract percentages; for homeowners, appreciation has been accelerating rapidly since fall 2025 as the effects of the AI startup boom ripple through the market.

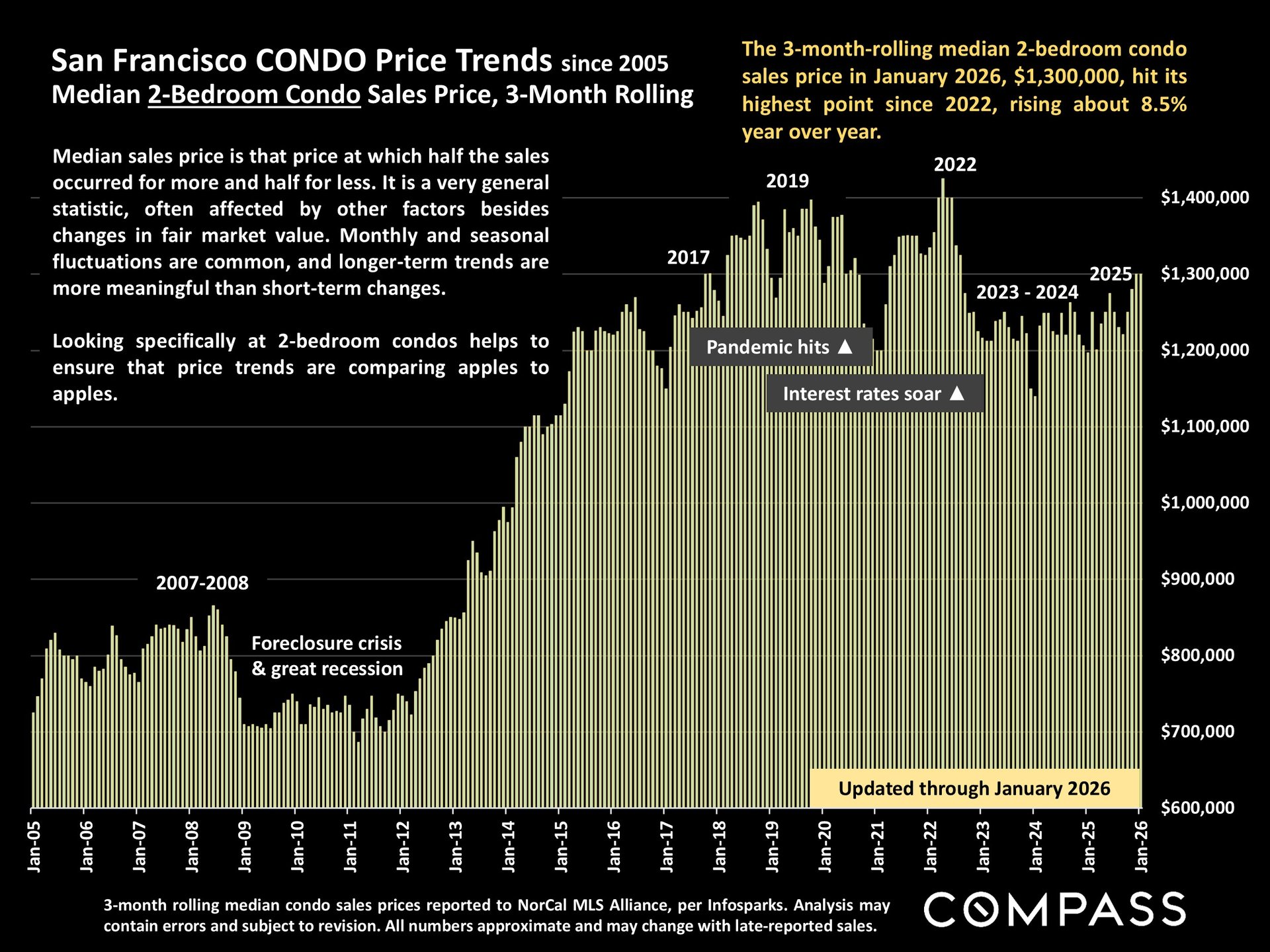

Yes—and the rebound is accelerating. The condo market, which took a significant hit during the pandemic years, is now showing real momentum. The median 2-bedroom condo price reached $1.3 million in January, its highest point since 2022, rising about 8.5% year over year. For buyers considering luxury condos in neighborhoods like South Beach, Yerba Buena, or Mission Bay, this trend is worth watching closely.

“The condo recovery has been one of the most encouraging stories over the last two years. With rents in rapid ascent from the influx of young AI workers, and the house market becoming almost impossibly competitive, more buyers are looking at condos as a compelling entry point into San Francisco’s luxury market.

That said, the condo market still shows the lingering effects of the pandemic. Compared to 2019, the overall median condo price is actually down about 5%. But the trajectory has clearly reversed, and with appreciation accelerating since fall 2025, the gap is narrowing quickly.

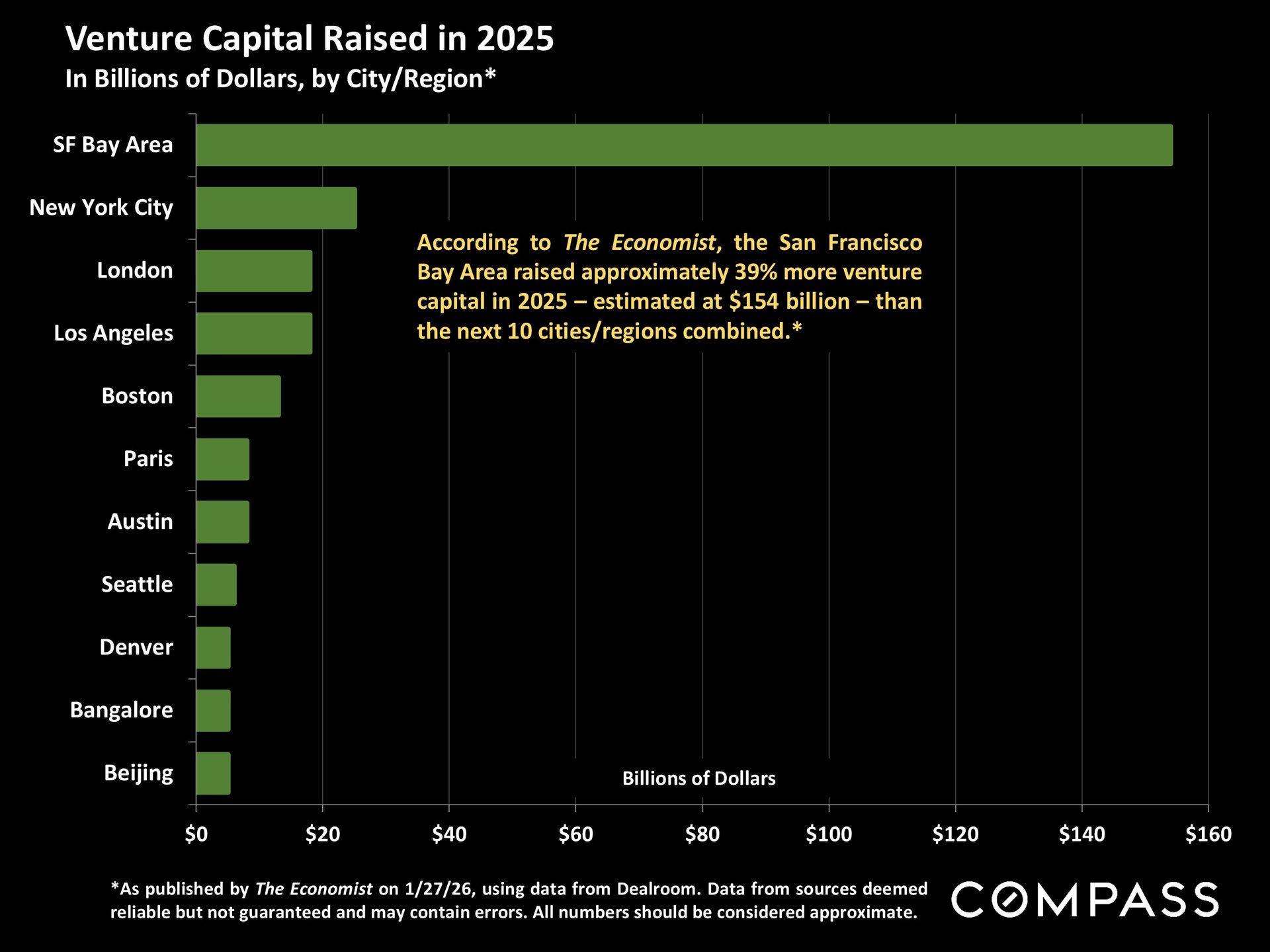

Nationally, those lower mortgage rates are gently nudging demand higher. In San Francisco, those same rates are colliding with something much more powerful: the AI startup boom. According to The Economist, the Bay Area raised an estimated $154 billion in venture capital in 2025—roughly 39% more than the next ten cities combined. That staggering concentration of capital is translating directly into housing demand, particularly from affluent buyers who are less sensitive to interest rate fluctuations.

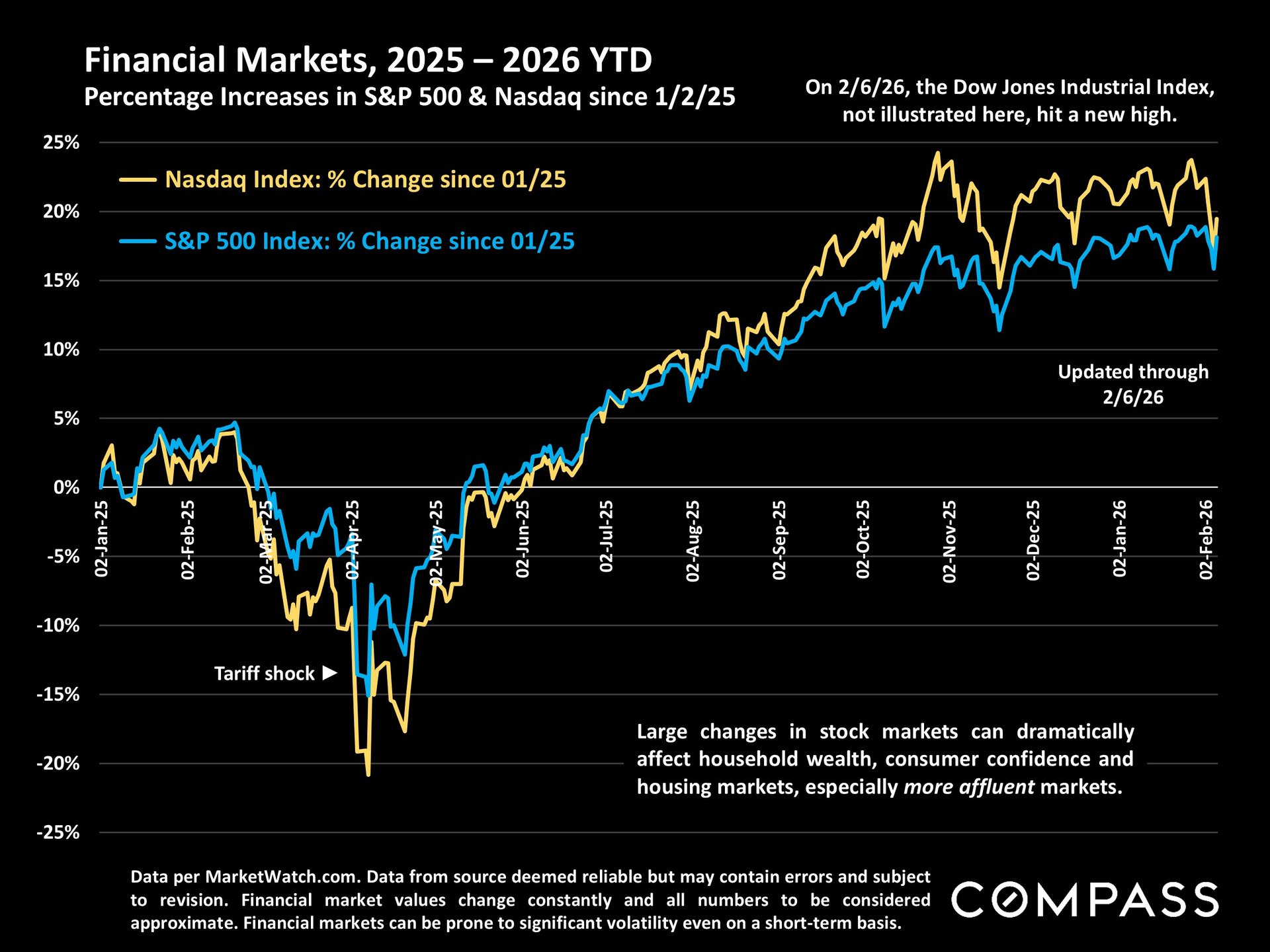

Stock markets remain near all-time highs—the Dow Jones Industrial Index hit a new record in early February—and local AI startup valuations continue to climb, generating substantial employee wealth. Rents have also been rising rapidly with the influx of young high-tech workers eager to work in AI, a demand signal that feeds directly into the for-sale market.

“As has been the case for the past two years, more affluent buyers are playing an outsized role in demand. These are buyers with significant equity positions in AI companies, stock market gains, and the financial confidence to move quickly. When you combine that with an extremely inadequate supply of homes, you get the kind of price surges we’re seeing.

In many parts of the country, the spring real estate market kicks off in April. In the Bay Area, it often starts in February. With new listings in January already down 19% year over year and buyer demand surging, all the conditions are in place for a very heated spring market. Houses are already averaging 27 days on market, and competitive bidding has become the norm across most price segments.

“We anticipate one of the most competitive spring markets in recent memory. Buyers who are waiting for more inventory may find that the listings that do come on the market get absorbed almost immediately. If you’re actively searching, the time to engage seriously is now—not April.

National median home prices are up approximately 1% year over year. San Francisco’s 3-month rolling median house price is up 12.4%, and on a single-month basis, it surged over 16%. The gap is driven primarily by the AI startup boom and an extremely low supply of available homes.

Several factors are converging: new listings in January were down 19% year over year, buyer demand is rapidly absorbing what does come on the market, and many potential sellers are staying put due to favorable existing mortgage rates. As of February 1, only 651 homes were listed citywide—down 27% from a year ago.

The Bay Area raised an estimated $154 billion in venture capital in 2025—39% more than the next ten cities combined. This wealth is creating a large pool of affluent buyers, rising rents from young tech workers, and a demand surge that is largely insulated from the factors slowing the national market.

The condo market is showing strong recovery momentum, with the median 2-bedroom price reaching $1.3 million—its highest since 2022 and up 8.5% year over year. With the house market extremely competitive (75% selling over asking), condos represent a potentially more accessible path into the market, particularly as appreciation accelerates.

As of early February 2026, the 30-year fixed conforming rate averaged 6.11% per Freddie Mac—near its 2-year low. While these rates are nudging demand higher nationally, in San Francisco their impact is amplified by AI-driven wealth. Many affluent buyers in the city are less rate-sensitive, making cash or large-down-payment offers that sidestep rate concerns entirely.

In the Bay Area, the spring market often starts in February rather than April. Given the current dynamics—extreme inventory shortage, surging demand, and 75% of houses selling over asking—the window from February through May typically produces the strongest results. Sellers who list early in the spring cycle often benefit from less competition among listings.

Whether you’re actively searching, considering listing, or just trying to make sense of how these numbers apply to your specific neighborhoods and price range, a conversation can make all the difference. What does the gap between national headlines and local reality mean for your goals?

📞 Call or text: (415) 704-3640

📅 Schedule a consultation: Book a time to discuss your goals

As a Global Luxury Specialist with Compass, I specialize in San Francisco’s premier neighborhoods including Pacific Heights, Russian Hill, Nob Hill, South Beach, Yerba Buena, Mission Bay, and Lower Pacific Heights. With a background in luxury hospitality and deep expertise in the Bay Area market, I help buyers and sellers navigate San Francisco’s most competitive segments.

Data Sources:

Primary phone

(415) 704-3640License Number

#02056250Address

891 Beach St,Sean Mamola is a San Francisco real estate agent who specializes in luxury properties and penthouses throughout the city's most coveted neighborhoods. As a Global Luxury Specialist with Compass and Rises.co, Sean works with discerning clients who are buying and selling exceptional properties in San Francisco. Since 2018 he has closed 75+ transactions and more than $100M in sales volume across the city's high-rise condo and penthouse market.

Sean focuses on San Francisco's premier areas including South Beach, Yerba Buena, Mission Bay, Pacific Heights, Lower Pacific Heights, Russian Hill, and Nob Hill. His deep knowledge of these neighborhoods allows him to guide clients to properties that perfectly match their lifestyle and investment goals.

Whether you're drawn to the modern luxury of South Beach condos, the urban sophistication of Yerba Buena, the waterfront appeal of Mission Bay, the timeless elegance of Pacific Heights, the historic charm of Russian Hill, or the prestigious heights of Nob Hill, Sean understands what makes each area unique.

For Sellers

Sean creates comprehensive marketing strategies that attract qualified buyers with refined tastes. He believes in elegant staging with meticulous attention to detail, ensuring your property makes an unforgettable impression. His marketing reaches both international and local luxury markets, maximizing exposure for condos, penthouses, condotels, and new developments.

For Buyers

Using cutting-edge technology and market research, Sean carefully analyzes pricing and property trends to find homes that satisfy his clients' specific preferences, price points, and lifestyles. His 24/7 availability and white-glove service ensure you never miss the right opportunity.

Working with Sean and his partnership with Rises.co gives clients significant competitive advantages. His vast network of interconnected agents results in winning offers and an impressively low ratio of properties shown to offers accepted. Sean's impeccable work ethic and precise negotiation skills ensure sellers find the right buyer and buyers secure their dream home.

Before becoming a licensed real estate agent, Sean spent years in luxury hospitality, skills he applies to every client relationship and transaction. He has tremendous respect for people's privacy and consistently exceeds expectations – from international travel to execute transactions to handling unique special requests.

As a Bay Area native who lived in New York City for 15 years, Sean brings a global perspective and genuine appreciation for people from all walks of life. His diverse background helps him connect with clients whether they're local San Francisco residents or international buyers seeking their perfect property.

When not working, Sean enjoys cycling, spending time with his large Irish-Italian family, and volunteering for Food Runners, The Richmond/Ermet Aid Foundation (REAF), and Broadway Cares/Equity Fights AIDS. This community involvement reflects his commitment to giving back to the city he serves.

If you're looking for an exceptional San Francisco real estate agent who specializes in luxury properties and provides truly high-touch service, let's talk. Sean is ready to help you find your perfect San Francisco home or achieve the best possible outcome when selling your property.

Specializing in luxury condos, penthouses, and exceptional properties in South Beach, Yerba Buena, Mission Bay, Pacific Heights, Lower Pacific Heights, Russian Hill, and Nob Hill.

Stay up to date on the latest real estate trends.

Sean Mamola | July 29, 2026

How Fillmore and Japantown condos are selling in 2026, for sellers.

Sean Mamola | July 28, 2026

Central, cultural, and mid-value: Fillmore and Japantown condos in 2026.

Sean Mamola | July 27, 2026

Deciding whether to sell or lease your Mission Bay condo? Compare market demand, HOA rules, taxes, and local costs to choose wisely.

Sean Mamola | July 26, 2026

Compare Mission Bay and SOMA condos for first-time buyers in San Francisco, from pricing and transit to lifestyle and inventory.

Sean Mamola | July 24, 2026

How Lower Pacific Heights condos are selling in 2026, for sellers.

Sean Mamola | July 23, 2026

What buyers should know about Lower Pacific Heights condos in 2026.

Sean Mamola | July 22, 2026

How Van Ness / Civic Center condos are selling in 2026, for sellers.

Sean Mamola | July 21, 2026

San Francisco's central value high-rise corridor, decoded for 2026 buyers.

Sean Mamola | July 16, 2026

When a condo loan stalls, it is usually the building, not the borrower. Here is how to get ahead of it.

CONTACT SEAN MAMOLA AT RISES.CO

CA DRE# 02056250

891 Beach St.,

San Francisco CA 94109